Finding the best house loan interest rates in Malaysia can be challenging, particularly with the numerous options available.

Critical terms such as home loan, housing loan, and loan tenure are essential for making informed decisions.

This guide will help you navigate the various loan types, their interest rates, and other key factors to consider when searching for your dream home.

In June 2026, several financial institutions in Malaysia offered competitive home loans and other financing options. Here’s a quick overview:

1. Best Housing Loan Rates in June 2026

| Bank Name | House Loan Name | Interest / Profit Rate | Financing Type | Tenure | Lock-In Period |

|---|---|---|---|---|---|

| MBSB | Property Refinancing-i and Remortgage-i | from 2.75% p.a. | Full Term islamic financing | Up to Year | None |

| Hong Leong | Housing Guarantee Scheme | from 2.75% p.a. | Term loan | Up to 35 years | None |

| Maybank Islamic | HouzKEY | from 2.88% p.a. | Term Islamic financing | Up to 35 years | 1 Year |

| Bank Islam | Baiti Home Financing-i | from 3.55% p.a. | Term Islamic financing | Up to 35 years | None |

| Bank of China | Housing Loan | from 3.88% p.a. | Term loan | Up to 35 years | 3 Years |

These banks offer a range of housing and home loans that cater to different needs, whether you’re looking for a flexible or a term loan.

Understanding Housing Loan Rates:

1. MBSB Property Refinancing-i and Remortgage-i

MBSB Property Refinancing-i and Remortgage-i are Islamic refinancing and remortgage facilities for homeowners who want to refinance their property or take cash out, using their home as collateral.

It offers a floating profit rate of 2.75% p.a., a financing margin of up to 90%, and no processing fee. The Product Disclosure Sheet also states that the facility is based on Tawarruq, and the monthly installment may change if the SBR/OPR changes.

a. Requirements

| Requirement | Description |

|---|---|

| Minimum Age | 18 to 65 years old |

| Who Can Apply | Any nationality |

| Employment Type | Salaried employees and self-employed applicants are eligible |

| Financing Type | Full-term Islamic financing |

| Profit Type | Floating profit rate |

| Profit Rate | From 2.75% p.a. |

| Profit Rate Ceiling | Capped at 11% p.a. |

| Margin of Finance | Up to 90% |

| Security Required | The property will be used as security for the financing |

| Tenure | Up to a year |

b. Fees & Charges

| Fees & Charges | Description |

|---|---|

| Processing Fee | No processing fee |

| Compensation Charge | 1% per annum Ta’widh compensation charge will be imposed on the outstanding installment amount |

| Redemption Letter Fee | RM50 per request |

| Letter for EPF Withdrawal Fee | RM50 per request |

| Credit Takaful | Required from MBSB Bank’s panel Takaful provider or another approved Takaful provider |

| Additional Security | Term Deposit-i may be requested depending on credit assessment |

c. Benefits

| Benefit | Description |

|---|---|

| Low Starting Profit Rate | Offers a starting profit rate from 2.75% p.a., which is one of the lowest among the listed bank loan options |

| High Financing Margin | Allows financing of up to 90%, which can help homeowners access more value from their property |

| Islamic Financing Structure | Based on the Shariah concept of Tawarruq, suitable for borrowers looking for Islamic refinancing |

| No Processing Fee | Helps reduce upfront application cost |

| Suitable for Refinancing or Remortgage | Useful for homeowners who want to restructure their existing property loan or access cash from their property value |

| Open to More Applicants | Available to any nationality, including salaried employees and self-employed applicants |

For more information, please visit the MBSB Bank website.

MBSB Property Refinancing-i and Remortgage-i Product Disclosure Sheet

2. Hong Leong Housing Guarantee Scheme

The Hong Leong Housing Guarantee Scheme is a government-guaranteed home loan under SJKP for eligible first-time Malaysian home buyers, including salaried employees and non-fixed-income earners. It offers financing of up to 100%, with interest rates from 2.75% p.a. and tenure up to 35 years.

The Product Disclosure Sheet states that this facility is calculated on a variable-rate basis, and that the property will be used as security for the bank.

a. Requirements

| Requirement | Description |

|---|---|

| Minimum Age | 18 years old |

| Who Can Apply | Malaysians only |

| Buyer Type | First-time home buyers |

| Employment Type | Salaried employees and self-employed applicants |

| Income Type | Suitable for fixed-income and non-fixed-income earners, including gig workers, traders, farmers, and fishermen |

| Property Purpose | Property must be for own occupation |

| Eligible Property Type | New, sub-sale, auctioned, completed or under-construction residential properties |

| Not Eligible | Land purchase or construction financing |

| Loan Type | Term loan |

| Interest Type | Floating interest rate |

| Interest Rate | From 2.75% p.a. for borrowing up to RM500,000 |

| Margin of Finance | Suitable for fixed-income and non-fixed-income earners, including gig workers, traders, farmers and fishermen |

| Maximum Financing Amount | Up to RM500,000, inclusive of MRTA/MRTT, LTHO, solicitor’s fees and valuation fees |

| Tenure | Up to 35 years |

| Credit Condition | Total monthly loan repayment should not exceed 65% of gross monthly income |

| Credit Record | CCRIS should not show arrears of more than 2 months within any 12-month period, with no adverse credit record within the last 24 months |

| Income Documents for Non-Fixed Income Earners | Bank statements, business license, fisherman’s registration card, or confirmation letter from authorized bodies such as JKKK, Penghulu, Category A government servants or elected representatives |

b. Fees & Charges

| Fees & Charges | Description |

|---|---|

| Processing Fee | Waived, subject to change |

| Early Settlement Fee | Not applicable because there is no lock-in period |

| Late Payment Fee | 1% p.a. on the outstanding amount in arrears |

| Escalating Late Charges | Additional charges may apply for repeated or prolonged default |

| Withdrawal Fee | Not applicable because this is a term loan |

| Redemption Letter Fee | RM50 per request |

| Letter for EPF Withdrawal Fee | RM20 per request |

| Insurance or Takaful Coverage | Required for residential properties under houseowner policy or takaful coverage, according to the PDS |

| Government Taxes | All fees are subject to prevailing government taxes where applicable |

c. Benefits

| Benefit | Description |

|---|---|

| Low Starting Interest Rate | Offers interest rates from 2.75% p.a., making it one of the lowest options in the provided list |

| Up to 100% Financing | Helps eligible buyers reduce the need for a large upfront deposit |

| Suitable for Non-Fixed Income Earners | Designed for applicants who may not have formal payslips, such as gig workers, small traders, farmers and fishermen |

| Government Guarantee Support | Backed by SJKP, which helps eligible applicants access financing even if they may not qualify through normal loan channels |

| Long Loan Tenure | Tenure of up to 35 years can help reduce monthly repayment pressure |

| Two-Generation Financing | Allows a child to join as a borrower to extend the loan tenure, subject to approval |

| No Lock-In Period | Borrowers can settle the loan early without early redemption or settlement fee |

| Financing Can Include Related Costs | MRTA/MRTT, LTHO, solicitor’s fees and valuation fees can be included within the RM500,000 financing ceiling |

| First-Home Buyer Friendly | Suitable for Malaysians buying their first home for own stay |

| Multiple Repayment Channels | Repayment can be made through standing instruction, HLB Connect, IBG transfer, ATM transfer, deposit machine or branch counter |

For more information, please visit the Hong Leong Bank website.

Hong Leong Housing Guarantee Scheme Product Disclosure Sheet

3. Maybank Islamic HouzKEY

Maybank Islamic HouzKEY is an Islamic homeownership solution designed to help Malaysian buyers own a home with a lower upfront cost and greater cash-flow flexibility. It offers up to 100% financing, no down payment, and a profit rate from 2.88% p.a., with a tenure of up to 35 years or until age 70, whichever comes earlier.

The Product Disclosure Sheet states that HouzKEY is based on the Shariah concept of Ijarah Muntahiyah Bi Tamlik, a lease contract that ends with ownership transferred via sale.

a. Requirements

| Requirement | Description |

|---|---|

| Minimum Age | 18 to 70 years old |

| Who Can Apply | Malaysian citizens only |

| Buyer Type | Suitable for first and second home Malaysian buyers |

| Home Financing Limit | Applicant must not have more than one home financing, including HouzKEY, at the point of application |

| Employment Type | Salaried employees and self-employed applicants |

| Guarantors | Up to 3 guarantors are allowed |

| Guarantor Requirement | Guarantors must be immediate family members, such as spouse, parents, siblings, or children |

| Guarantor Age | Guarantors must be between 18 to 70 years old |

| Financing Type | Term Islamic financing |

| Profit Type | Floating profit rate |

| Profit Rate | From 2.88% p.a. |

| Eligible Property Price | RM250,000 to RM2,000,000 |

| Margin of Finance | Up to 100% |

| Tenure | Initial tenure of 5 years, with flexibility to continue up to another 30 years |

| Maximum Tenure | Up to 35 years, or up to age 70, whichever is earlier |

| Eligible Locations | Selected projects in Kuala Lumpur, Selangor, Johor and Penang |

| Eligible Property Type | Selected properties from Maybank’s partnering developers, including new launches, under-construction and completed properties |

b. Fees & Charges

| Fees & Charges | Description |

|---|---|

| Processing Fee | No fee |

| Down Payment | No down payment required |

| Security Deposit | 3 months refundable security deposit is required upon signing the HouzKEY Agreements and SPA |

| Early Settlement Fee | No fee |

| Compensation Charge | 1% p.a. on the outstanding amount |

| Late Payment Charges | 1% p.a. on the monthly payment amount in arrears or any other approved amount by BNM |

| Legal Fees for SPA | Legal fee based on the Solicitor’s Remuneration Order and disbursement, if not absorbed by the developer |

| Stamp Duty for SPA | Nominal stamp duty of RM10 per copy, with four copies to be stamped |

| Legal Fees for Home Financing Agreement | Legal fee based on the Solicitor’s Remuneration Order and disbursement |

| Stamp Duty for Home Financing Agreement | Based on Stamp Act requirement for the original copy, with RM10 nominal stamp duty for each duplicate copy |

| Legal Fees for Deed of Trust | RM300 |

| Legal Fees for Power of Attorney | RM300 |

| Legal Fees for Purchase Undertaking | RM150 |

| Notice of Settlement | RM50 |

| Property Maintenance Costs | Utilities, fire takaful, quit rent, assessment fee, maintenance fee and other related property payments are borne by the buyer during the tenure, where applicable |

| Takaful Coverage | Fire Takaful is encouraged, while Family Takaful or Life Insurance is optional but recommended |

c. Benefits

| Benefit | Description |

|---|---|

| 100% Financing | Allows eligible buyers to finance the full property price without a down payment |

| Lower Upfront Cost | Buyers only need to prepare a 3-month refundable security deposit, subject to terms and conditions |

| No Payment During Construction | Buyers do not need to make payment during the construction period until the key or vacant possession is handed over |

| Low Starting Profit Rate | Offers a profit rate from 2.88% p.a., subject to Maybank’s approval and assessment |

| Flexible Tenure | Starts with a 5-year initial tenure and can be extended up to another 30 years |

| Cash Flow Friendly | Monthly payment during the initial tenure is structured as profit payment only, helping reduce monthly payment pressure |

| Up to 3 Guarantors Allowed | Applicants can strengthen their application by including up to 3 immediate family members as guarantors |

| Suitable for New or Under-Construction Homes | Available for selected new launches, under-construction and completed properties from participating developers |

| Option to Continue After Initial Tenure | Buyers may continue with HouzKEY after the initial tenure without paying a new down payment, subject to the bank’s terms |

| Option to Buy, Refinance or Sell | After fulfilling the required period, buyers may buy the property, refinance with Maybank Islamic or other banks, or sell the property to settle the outstanding amount |

Visit Maybank website for more information

Maybank Islamic HouzKEY Product Disclosure Sheet

4. Bank Islam Baiti Home Financing-i

Bank Islam Baiti Home Financing-i is an Islamic home financing facility for Malaysians who want to buy a residential property, whether under construction or completed.

It is based on the Tawarruq Shariah concept, with a floating effective profit rate of up to 3.55% p.a., a financing margin of up to 90%, no processing fee, and no lock-in period. The Product Disclosure Sheet also states that the financing is for residential property purchase, with the Effective Profit Rate calculated on a variable or floating rate basis

a. Requirements

| Requirement | Description |

|---|---|

| Minimum Annual Income | RM24,000 |

| Minimum Age | 18 to 70 years old |

| Who Can Apply | Malaysians only |

| Employment Requirement | Applicant should be employed or own a business for at least 3 years |

| Credit Requirement | Applicant should not be bankrupt or involved in legal action |

| Payment Track Record | Minimum 1 year of good payment track record |

| Financing Type | Term Islamic financing |

| Shariah Concept | Tawarruq |

| Profit Type | Floating profit rate |

| Profit Rate | From 3.80% p.a. for property value above RM300,000 |

| Rate for Property RM300,000 and Below | From 4.10% p.a. |

| Margin of Finance | Up to 90% |

| Tenure | Up to 35 years |

| Approval Time | Around 30 days, subject to Bank Islam’s approval |

| Eligible Property | Residential property, including under-construction or completed property |

| Collateral | The financed property will be used as collateral |

| Guarantor | May be required on a case-by-case basis, depending on credit assessment |

| Required Takaful | MRTT or MLTT is compulsory |

| Optional Takaful | Houseowner or Householder Takaful Plan, if applicable |

b: Fees & Charges

| Fees & Charges | Description |

|---|---|

| Processing Fee | Waived |

| Early Settlement Fee | No lock-in period. Bank Islam shall grant Ibra’ on deferred profit after full settlement |

| Compensation Charge | 1% p.a. on overdue installments before maturity until full payment |

| Charge After Maturity | Based on the prevailing daily overnight Islamic Interbank Money Market Rate on the outstanding balance |

| Redemption Letter Fee | RM50 per request |

| Letter for EPF Withdrawal Fee | RM20 per request for manual application, RM10 per request for online application |

| Stamp Duty | Based on Stamp Duty Act 1949 |

| Disbursement Fee | Includes registration of charge and other related charges |

| Valuation Fee | Applicable for completed property or own construction by appointed contractor |

| Wakalah Fee | RM25 for Appointment of the Bank as Purchase Agent and RM25 for Appointment of the Bank as Sales Agent |

| Legal Fees | Legal fees and incidental expenses related to security documentation |

| Custodian Fee | RM80 annually for safekeeping of security documents after the facility is fully settled |

| Copy of Security Documents | RM50 per request |

| Cancellation Fee | Customer must pay costs incurred by the bank for preparation and registration of security documents, if the facility is canceled |

| Takaful Contribution | Based on the contribution amount required by the Takaful operator |

| MRTT or MLTT | Compulsory coverage for the financing facility |

| Houseowner or Householder Takaful | Applicable if required |

c. Benefits

| Benefit | Description |

|---|---|

| Competitive Profit Rate | Offers a profit rate from 3.80% p.a. for property value above RM300,000 |

| High Financing Margin | Allows financing of up to 90% of the property value |

| Long Financing Tenure | Tenure of up to 35 years can help make monthly installments more manageable |

| No Processing Fee | Reduces upfront application cost for borrowers |

| No Lock-In Period | Borrowers can settle the financing early without being tied to a lock-in period |

| No Early Settlement Penalty | Bank Islam grants Ibra’ on deferred profit after full settlement |

| Islamic Financing Structure | Suitable for buyers looking for Shariah-compliant home financing based on Tawarruq |

| Suitable for New and Completed Homes | Can be used for residential properties that are under construction or already completed |

| Step Up Payment Scheme | Available for eligible first-time home buyers, allowing them to pay only the profit portion during the Step Up period |

| Profit Rate Protection | The Bank’s Sale Price is based on the Ceiling Profit Rate, while the Effective Profit Rate is floating |

| Takaful Protection | MRTT or MLTT helps protect the borrower and family in the event of death or total permanent disability |

You may visit the Bank Islam website for more information.

Bank Islam Baiti Home Financing-i Product Disclosure Sheet

5. Bank of China Housing Loan

Bank of China Housing Loan is a conventional term loan for buyers who want to finance a completed or under-construction residential property in Malaysia, or refinance an existing housing loan. It offers a floating interest rate from 3.88% p.a., with financing margin of up to 90% and tenure of up to 35 years.

The Product Disclosure Sheet states that the Housing Loan is a secured loan, and the residential property will be used as security to the bank.

a. Requirements

| Requirement | Description |

|---|---|

| Minimum Annual Income | RM60,000 |

| Minimum Monthly Income | RM5,000 |

| Minimum Age | 18 to 70 years old |

| Who Can Apply | Malaysians, permanent residents and foreigners working in Malaysia |

| Foreigner Requirement | Foreigners must have valid passport, visa, work permit or employment pass |

| Employment Type | Salaried employees and self-employed applicants |

| Loan Type | Term loan |

| Interest Type | Floating interest rate |

| Interest Rate | From 3.88% p.a. |

| Loan Amount | Minimum loan amount from RM300,000 |

| Eligible Borrowing Range | More than RM300,000 |

| Margin of Finance | Up to 90% of the SPA price or market value |

| Tenure | Up to 35 years |

| Lock-In Period | 3 years |

| Eligible Property | Residential property, including completed or under-construction property |

| Refinancing Option | Can be used to refinance an existing housing loan |

| Security Required | The residential property will be used as security for the loan |

b. Fees & Charges

| Fees & Charges | Description |

|---|---|

| Processing Fee | No processing fee |

| Stamp Duty | Payable according to the Stamp Act 1949 |

| Late Payment Fee | 1% p.a. on the amount in arrears, causing the total outstanding amount to increase |

| Early Settlement Fee | 2.25% on the prepayment amount if prepayment or full settlement is made within the first 3 years from the first loan release date |

| Setup Fee | One-time setup fee may apply: RM50 for loan up to RM30,000, RM100 for RM30,001 to RM100,000, and RM200 for RM100,000 and above |

| Monthly Maintenance Fee | RM10 per month applies only to Flexi Housing Loan or Flexi Term Loan |

| Fire Insurance | Mandatory. The property must be adequately insured against risk for its full value or replacement cost, whichever is higher |

| Houseowner Insurance | Optional |

| MRTA | Optional but encouraged |

| MLTA | Optional but encouraged |

| Legal or Insurer Choice | Borrower may use the bank’s panel lawyers or insurers, or appoint their own lawyer or insurer |

c. Benefits

| Benefit | Description |

|---|---|

| Competitive Interest Rate | Offers interest rate from 3.88% p.a., subject to Bank of China’s approval |

| Long Loan Tenure | Tenure of up to 35 years can help make monthly instalments more manageable |

| High Financing Margin | Financing margin of up to 90% helps buyers reduce upfront capital needed |

| Suitable for Purchase or Refinancing | Can be used to finance residential property purchase or refinance an existing housing loan |

| Available for Under-Construction Property | Buyers can use this loan for completed or under-construction residential properties |

| Open to More Applicant Groups | Available to Malaysians, permanent residents and foreigners working in Malaysia |

| No Processing Fee | Helps reduce the initial cost of applying for the housing loan |

| Optional MRTA or MLTA | Borrowers are encouraged to take MRTA or MLTA for protection in the event of death or total permanent disability |

| Flexi Option Available | The PDS mentions Flexi Housing Loan options, which allow deposit and withdrawal flexibility with interest savings through a linked current account |

| Choice of Lawyers or Insurers | Borrowers can choose the bank’s panel lawyers or insurers, or appoint their own, subject to bank requirements |

Visit Bank of China for more information

Bank of China Housing Loan Product Disclosure Sheet

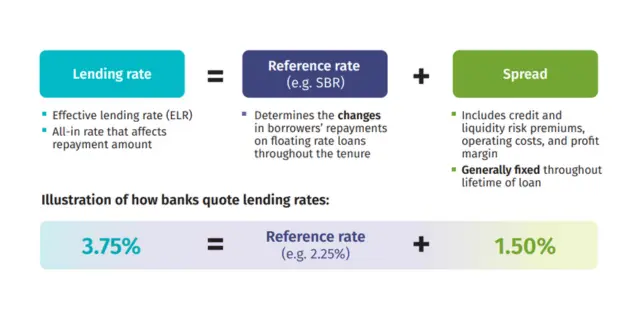

2. Understanding the Effective Lending Rate (ELR)

The Effective Lending Rate (ELR) is a critical component when evaluating home loans. It represents the total cost of borrowing, expressed as an annual percentage rate. The ELR includes the reference rate and the spread, which collectively impact your monthly repayments.

- Reference Rate: The base rate, such as the Standardised Base Rate (SBR), is influenced by Bank Negara Malaysia’s policies.

- Spread: Additional charges include credit and liquidity risk premiums, operating costs, and the bank’s profit margin.

The ELR is crucial because it affects the total repayment amount and helps borrowers effectively compare different loan products.

What is the Reference Rate?

The reference rate is a benchmark interest rate used by Malaysian banks to determine changes in borrowers’ repayments on floating-rate loans over the loan tenure.

This rate can vary across institutions, but it serves as a foundation for setting the lending rate.

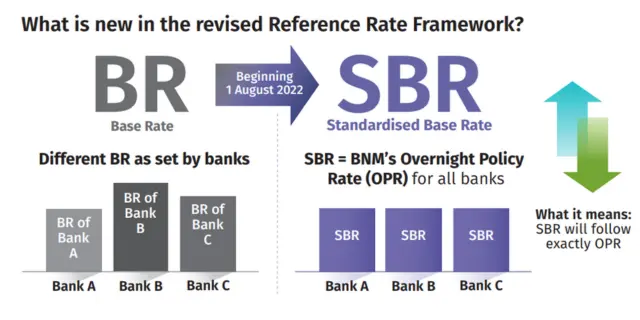

Is the Reference Rate Equal to the Standardised Base Rate (SBR)?

No, the reference rate differs from the Standardised Base Rate (SBR). The SBR is a specific reference rate that standardizes the base rate across all banks.

Introduced on 1 August 2022, the SBR is directly linked to the Overnight Policy Rate (OPR) set by Bank Negara Malaysia.

This standardization aims to simplify comparing loan rates across banks.

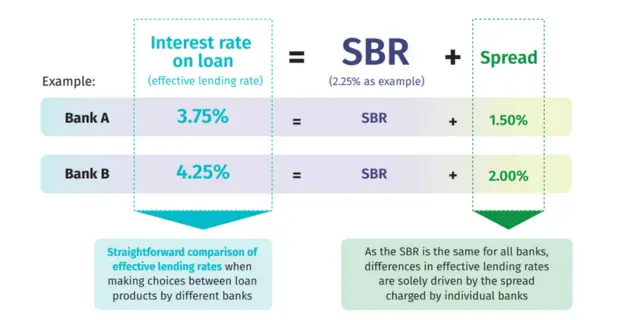

Is the Reference Rate Equal to the Overnight Policy Rate (OPR)?

The reference rate may include the OPR, especially when the SBR is used.

The OPR is the interest rate at which banks lend to each other overnight and is set by the central bank.

Changes in the OPR directly affect the SBR and the reference rate used for loans.

What is Spread?

The spread is an additional percentage added to the reference rate to arrive at the ELR. It covers various costs and risks incurred by the bank, including:

- Credit Risk Premium: Compensation for the risk that a borrower might default.

- Liquidity Risk Premium: Compensation for the risk associated with the bank’s liquidity.

- Operating Costs: The day-to-day expenses of running the bank.

- Profit Margin: The bank’s earnings from the loan.

The spread is generally fixed for the duration of the loan unless there is a significant change in the borrower’s credit risk profile.

3. Understanding House Loan Interest Rates

Understanding the mechanics of interest rates and their impact on repayments is essential for making informed decisions about Malaysian home loans.

What are House Loan Interest Rates?

House loan interest rates are the percentage of the loan principal that banks charge.

These rates determine the cost of borrowing and are influenced by various factors, including the central bank’s policies and the individual bank’s cost structures.

How to Calculate House Loan Interest Rate?

Calculating your home loan interest rate is crucial for understanding the total amount you will pay over time.

Use a home loan calculator to determine your monthly instalments and total repayment. Here’s an example:

Example Calculation:

- Bank’s Base Rate (BR): 2.00%

- Spread: 1.50%

- ELR: BR + Spread = 2.00% + 1.50% = 3.50%

For a loan of RM300,000 over 30 years, the monthly instalment would include interest and principal repayments. Understanding these calculations can help you save money and manage your loan tenure effectively:

- Annual Interest Amount: RM300,000 x 3.50% = RM10,500

- Monthly Interest Amount: RM10,500 / 12 = RM875

Thus, the monthly repayment would include RM875 in interest plus the principal repayment.

What Can Affect Your House Loan Interest Rate?

Several factors can influence your house loan interest rate, including:

- Central Bank Policies: Changes to Bank Negara Malaysia’s Overnight Policy Rate (OPR) can directly affect interest rates.

- Economic Conditions: Inflation and economic stability can influence interest rates.

- Borrower’s Credit Score: Higher credit scores often result in lower interest rates.

- Loan Tenure: Longer loan tenures can sometimes attract higher interest rates.

4. How Should You Compare Lending Rates Across Banks as Borrowers?

Comparing lending rates across banks involves more than just looking at the ELR. Consider the following steps:

- Review the ELR and Spread: Compare the total borrowing cost.

- Understand Additional Fees: Be aware of any extra fees that might apply.

- Read the Product Disclosure Sheet (PDS): This document provides crucial details about the loan.

5. How to Plan and Compare Your House Loan Interest Rates?

When planning a home loan, consider the property’s value, the loan amount, and the loan tenure.

Use a loan calculator to estimate your monthly instalments and ensure you understand all associated fees.

Planning and comparing Malaysia house loan interest rates requires a strategic approach:

- Research Different Lenders: Identify potential lenders and their offerings.

- Interest Rates: Compare the interest rates offered by different banks.

- Additional Features: Evaluate foreclosure charges and other loan features. Some loans include extra funds withdrawal or linked current accounts for easier management.

- Read Reviews: Learn from the experiences of other borrowers.

- Seek Professional Advice: Consult with financial advisors if needed.

- Maximum Loan Tenure: Most banks offer up to 35 years.

- Prepayment Options: Check if the bank allows for additional payments without penalties.

- Insurance Requirements: Most housing loans require Mortgage Reducing Term Assurance (MRTA) or other types of insurance.

- Flexibility: Compare loans that offer flexible repayment options, like a flexi loan or semi-flexi loan (make sure to understand the terms and conditions).

Critical Terms in Home Financing

Understanding key terms related to home financing is crucial for navigating the market:

- Outstanding Principal Balance: The remaining amount you owe on your loan, excluding interest.

- Home Loan Balance: The total amount left to pay on your home loan.

- Basic Term Loan: A standard loan with fixed interest rates and repayment terms.

- Loan Period: The total time over which you will repay the loan.

- Mortgage Reducing Term Assurance: Insurance that decreases as your loan balance decreases.

Choosing the right home loan in Malaysia requires careful consideration of several factors, including interest rates, loan tenure, and associated fees.

By understanding the options available and using tools like a home loan calculator, you can make a more informed decision that aligns with your financial goals and helps you secure your dream home.

Are you looking for a dream house after getting the best house loan interest rates? We can assist you! Please send us your details, and we will contact you shortly.

Continue Reading: