| TL;DR Bank Negara Malaysia has kept the OPR steady at 2.75% as of January 2026. This is great news for borrowers because home loan interest rates remain stable, keeping monthly installments predictable. Inflation is manageable at around 1.4%, and the economy is growing. For buyers, it is a sweet spot to enter the market before demand drives prices up. If you are on a floating rate, your payments won’t spike. |

We know that finance jargon can be as dry as toast. But when Bank Negara Malaysia decides on the Overnight Policy Rate (OPR), it is basically deciding the “price tag” of the money in your pocket. FYI, as of 22 Jan 2026, the OPR remains at 2.75%.

You might be wondering, “Okay, but will this actually make buying a house cheaper for me, or is it just simple talk?” Whether you are a first-time or existing homebuyer or an investor, let’s sit down, grab a coffee, and break down exactly what this means for your wallet without the headache.

Key Takeaways

- Stability is King: BNM’s decision to keep the Malaysia OPR 2026 rate at 2.75% provides a predictable environment for financial planning.

- Lower Repayments: Borrowers with floating-rate loans continue to enjoy lower monthly installments compared to the historical high rates of the past.

- Buyer’s Market: With manageable financing costs, 2026 is shaping up to be an opportune time for property investment and first-time purchases.

- Focus on the Spread: Since the base rate is standard, your goal is to find the bank offering the lowest “spread” or profit margin.

How OPR Affects Homebuyers and Investors?

- 1. Why did Bank Negara Malaysia maintain OPR at 2.75%?

- 2. What Does OPR 2.75% Mean for Home Buyers in Malaysia?

- 3. How Does Bank Negara’s Interest Rate Decision Affect Housing Demand?

- 4. Is 2026 a Good Time to Buy Property in Malaysia?

- 5. Fixed vs Floating: What is the Best Strategy for Property Buyers in 2026?

- 6. FAQs Regarding Malaysia OPR in Early 2026

1. Why did Bank Negara Malaysia maintain OPR at 2.75%?

It often feels like a guessing game with the economy, but BNM’s move to hold the line at 2.75% is quite calculated. According to the Monetary Policy Statement by Bank Negara Malaysia on 22 Jan 2026, the global economy is actually doing a bit better than expected, thanks to lower tariffs and a tech boom driven by AI.

Here is the situation: BNM isn’t trying to slam the brakes (raise rates) or step hard on the gas (lower rates). They are “cruising.” Inflation in Malaysia in 2026 is hovering at a very modest 1.4%. If prices of goods aren’t skyrocketing, the central bank doesn’t need to make loans expensive to cool us down.

Let us give you an example: imagine the economy is a car. If it goes too fast (high inflation), you pull the handbrake (raise OPR). If it stalls, you push the gas (cut OPR). Right now, the car is driving smoothly at the speed limit. This stability is meant to keep the Ringgit steady and support domestic spending.

2. What Does OPR 2.75% Mean for Home Buyers in Malaysia?

This is the part where the rubber meets the road. A stable, relatively low OPR directly translates into greater mortgage repayment affordability in Malaysia. When the OPR is low, the banks’ cost of funds is low, and they pass (some of) that savings to you.

According to Kenneth Soh from PropertyGuru & iProperty, clear insights are critical right now. He notes that this rate is a timely boost. Let’s look at the numbers because they don’t lie.

a. Potential Monthly Savings Scenario (30-Year Loan)

Let’s say 2 different properties with 30-year mortgages with 3.8% with 90% financing:

| Property Value | RM 500,000 | RM 865,000 |

|---|---|---|

| Loan Amount (90%) | RM 450,000 | RM 778,500 |

| Interest Rate | 3.8% | 3.8% |

| Monthly Repayment | ~RM 2,097 | ~RM 3,627 |

| Monthly Repayment After OPR Cut | ~RM1,903 ( ↓ ~RM194/month) | ~RM3,295 ( ↓ RM332/month) |

| 30-year savings | RM194 × 360 ≈ RM69,840 | RM332 × 360 ≈ RM119,520 |

As you can see, a small percentage difference saves you thousands over a 30-year period. It essentially increases your “disposable income,” allowing you to spend that extra cash on renovations or savings.

For navigating these options, IQI Global offers a blend of data analytics and personalized service. Whether you are looking for Malaysia house loan advice or the perfect property, our network across 35+ countries means we have seen it all. Our technology helps you quickly match with the best options. Contact us now!

3. How Does Bank Negara’s Interest Rate Decision Affect Housing Demand?

When money is “cheap” (or at least, not expensive), people feel braver. It is basic behavioral science that when we feel financially secure, we are more likely to make big life decisions, like buying a home. The Ministry of Finance has explicitly stated that lower borrowing costs support homeownership affordability.

Currently, there is a vibe of “cautious optimism.” Malaysia’s standardized base rate remaining flat means developers are confident enough to launch new projects. We are seeing a shift where fence-sitters, people who were waiting for rates to drop, are realizing rates likely won’t drop further, so they are entering the market now before Malaysian property prices tick upward.

Consider the “wealth effect.” When your monthly installment is lower, you feel wealthier. You might buy better furniture or invest in a smart home system. This boosts the broader economy, not just real estate.

Looking to capitalize on this demand? IQI Global is a PropTech leader. Our 65,000 “Warriors” (agents) use the IQI Atlas SuperApp to provide real-time data, ensuring you never miss a hot listing, whether it’s a new launch or a secondary market gem. Contact us for more information!

4. Is 2026 a Good Time to Buy Property in Malaysia?

This is the million-ringgit question. With the Malaysian OPR steady, we are seeing what experts call a “Goldilocks” period: not too hot, not too cold. The Malaysian property cycle appears to be entering a recovery and growth phase.

Hartamas Real Estate notes that the economic footing is solid, supported by domestic demand. However, there is still an “overhang” of unsold units in some areas. This is actually good for you. Why? Because developers are still offering goodies (rebates, free legal fees) to clear stock, even as the interest rate environment improves.

a. Why 2026 might be your year!

- Cost of Entry: Financing is accessible.

- Inventory: There is plenty of choice in the market (Condos, landed, etc.).

- Stability: You don’t have to fear a sudden 1.0% rate hike next month.

However, don’t just buy because of F.O.M.O (Fear of Missing Out). Buy because the numbers work for you.

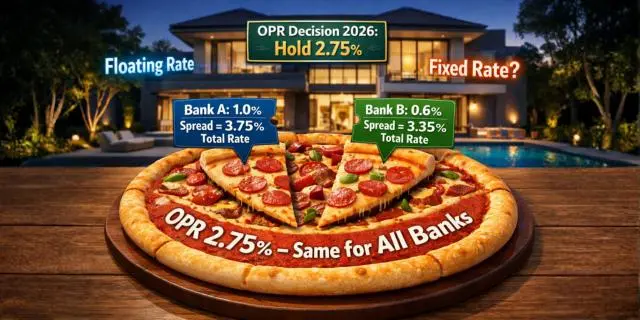

5. Fixed vs Floating: What is the Best Strategy for Property Buyers in 2026?

If you take a loan today, should you go with a fixed or a Floating rate? Most Malaysian loans are floating, meaning they move with the OPR. Since the Bank Negara Malaysia OPR decision in early 2026 is to hold steady, floating rates are currently very attractive.

Here is a pro-tip regarding the “Spread“. All banks now use the same SBR (Standardized Base Rate), which equals the OPR (2.75%). So, the only way banks compete is on the Spread.

Let’s give you an example: Think of a loan like a pizza.

- The Dough is the OPR (2.75%). Every bank has the same Dough.

- The Toppings are the Spread (Bank’s profit).

- One bank charges you 1.0% for toppings (Total 3.75%). Another charges 0.6% (Total 3.35%).

- Your Strategy: Shop for the cheapest toppings!

Since experts predict stability for the rest of 2026, a floating rate with a low spread is likely your best bet to minimize costs.

Confused by the paperwork? IQI Global is your one-stop solution! From valuation to finding the right banker, our comprehensive service model simplifies the journey. We transact tens of thousands of properties globally, so we know how to spot a good deal. Contact us for any real estate related question!

In summary, the decision to keep the Malaysian OPR at 2.75% acts as a steady hand on the economic tiller. For you, it removes the fear of volatility, making early 2026 a strategic year to secure fair home loan rates.

Remember, the market waits for no one, but with stable rates, at least you can plan your next move with clarity. Be smart, compare the “spread,” and look at the long term.

6. FAQs Regarding Malaysia OPR in Early 2026

a. Why did Bank Negara maintain OPR at 2.75%?

Bank Negara Malaysia maintained the OPR to support economic growth while keeping inflation in check (currently approx 1.4%). They aim to keep the Ringgit stable and ensure borrowing remains affordable for the Rakyat.

b. What Happens When OPR is Unchanged?

For existing borrowers with floating-rate loans, your monthly installments stay the same, no nasty surprises. For new buyers, it means housing affordability remains stable, allowing for better budget planning without fear of sudden rate hikes.

c. How OPR Affects Inflation and Property?

Generally, a lower/stable OPR encourages spending, which supports property demand. It keeps borrowing costs low, preventing the housing market from stalling, while keeping inflation moderate by not overheating the economy.

d. If OPR Stays at 2.75%, Should I Buy a House Now?

Yes, it is a favorable time. With interest rates stabilized and developers eager to sell, you can lock in a good financing rate. Waiting too long could lead to property prices rising as demand increases later in 2026.

e. Will My Mortgage Installment Increase in 2026?

It is unlikely to increase significantly. Most experts forecast the Malaysian OPR will remain at 2.75% for the year unless there is a major global economic shock.

f. Is Refinancing Smart When OPR is Stable?

Absolutely. If your current loan has a high “spread,” you can refinance to a new package that takes advantage of the competitive rates banks are offering right now.

g. Is Fixed Rate or Floating Rate Better in 2026?

A floating rate is generally preferred in this stable environment, provided you secure a low spread. Fixed rates offer peace of mind but usually start at a higher percentage than current floating rates.

Ready to take advantage of the stable OPR rates and find your dream home or investment? Contact us today to leverage our technology and global network for your real estate success!

Continue Reading:

- Philippines Property Market 2026: Where Global Investors Should Look

- Best Housing Loan Rates to Secure in February 2026

- Property Buying and Rental Price in Malaysia (2026 Global Guide)

Reference

- Abdul Jabbar, R. (2026, February 19). How OPR Affect Housing Loans in Malaysia? iProperty. Retrieved from

https://www.iproperty.com.my/guides/how-will-the-opr-increase-affect-your-home-loan-9395 - Azami, S. (2026, January 22). BNM kekalkan OPR pada 2.75 peratus. Astro Awani. Retrieved from

https://www.astroawani.com/berita-bisnes/bnm-kekalkan-opr-pada-275-peratus-556551 - Bank Negara Malaysia. (2026, January 22). Monetary Policy Statement. Retrieved from

https://www.bnm.gov.my/-/monetary-policy-statement-22012026 - Bank Negara Malaysia. (n.d.). OPR Decisions. Retrieved from

https://www.bnm.gov.my/monetary-stability/opr-decisions - Chua, S. (2025, July 9). BNM Cuts OPR to 2.75%: What It Means for Your Money. Ringgit Plus. Retrieved from

https://ringgitplus.com/en/blog/personal-finance-news/bnm-cuts-opr-to-2-75-what-it-means-for-your-money.html - Kaur, S. (2025, July 15). OPR cut to 2.75pct a timely boost for homebuyers, homeowners, developers. New Straits Times. Retrieved from

https://www.nst.com.my/property/2025/07/1244937/opr-cut-275pct-timely-boost-homebuyers-homeowners-developers#google_vignette - Ministry of Finance. (2025, September 10). Low OPR Reduces Borrowing Costs, Helps People Own Homes. Retrieved from

https://www.mof.gov.my/portal/en/news/press-citations/low-opr-reduces-borrowing-costs-helps-people-own-homes-mof - Tan, R. (2025, July 14). The 2025 OPR Cut: What It Means for Your Home Loan. Hartamas Real Estate. Retrieved from

https://hartamas.com/how-the-opr-affects-your-home-loan-interest-rates/