| TLDR: CP58 is a mandatory statement employers must issue to agents, dealers, and distributors who receive incentives or commission exceeding RM5,000 annually. It is not optional. Non-compliance may result in penalties under Malaysia’s Income Tax Act. |

If you run a business in Malaysia and pay commission, incentives, or performance bonuses, there’s one document you cannot afford to ignore: CP58.

Many employers only discover CP58 during audit season — and by then, it’s stressful.

Whether you’re a small business owner, HR executive, payroll officer, or simply trying to understand what CP58 is, this guide explains what it means, who must issue it, and how to stay compliant.

No tax jargon. Just clarity.

Key Takeaways

- CP58 is a record of commission or incentive income, not a tax bill.

- CP58 income is taxable and must be declared in Malaysia.

- The RM5,000 annual threshold determines mandatory issuance.

- Missing the 31 March deadline may expose companies to compliance risk.

- Understanding CP58 early reduces audit exposure and financial penalties.

Table of contents

What Is CP58 and Why It Exists

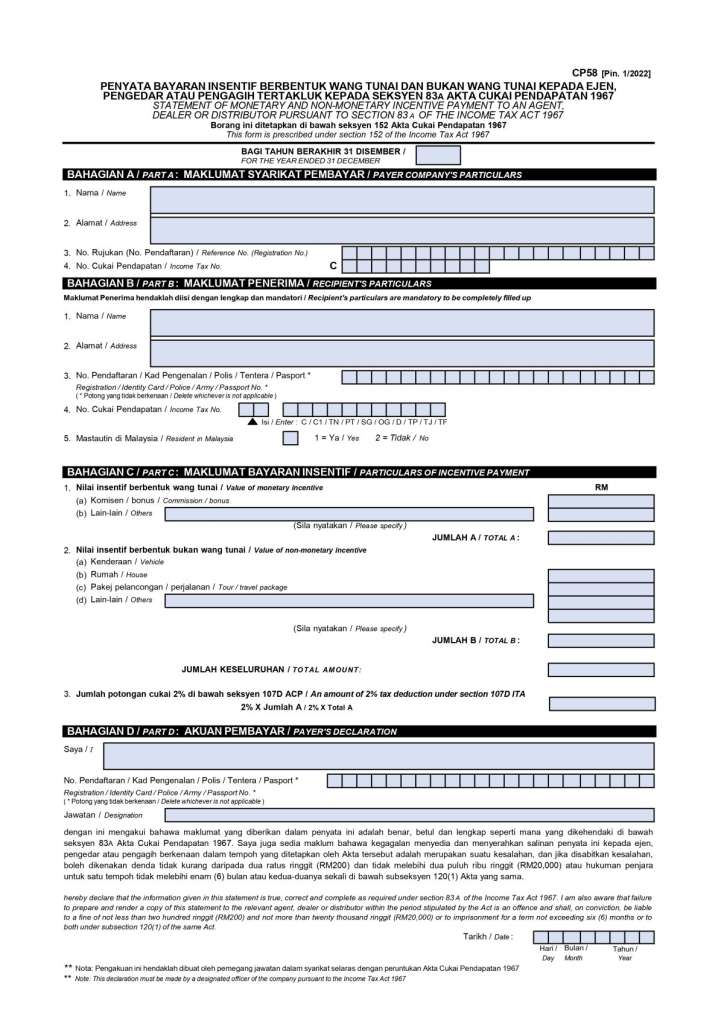

CP58 is a statement of monetary and non-monetary incentive payments made to agents, dealers, or distributors.

It is required under Section 83A of the Income Tax Act 1967 and regulated by Lembaga Hasil Dalam Negeri (LHDN)

Its purpose:

- Ensure incentive payments are recorded

- Support tax transparency

- Allow recipients to declare income correctly

CP58 is not issued to salaried employees. It applies specifically to non-employment incentive arrangements.

Who Must Issue CP58 in Malaysia?

An employer must issue CP58 if:

- The company pays monetary or non-monetary incentives

- The total incentive exceeds RM5,000 in a year

- The recipient is an agent, dealer, or distributor

- The recipient is not a salaried employee under normal payroll

This includes:

- Real estate agencies paying negotiator commissions

- Insurance companies paying agent bonuses

- Direct selling companies rewarding distributors

- Businesses providing referral incentives

If your company pays commission-based individuals outside standard payroll, CP58 likely applies.

When and How Employers Must Issue CP58

Deadline

CP58 must be issued before 31 March of the following year for incentives paid in the previous year.

Example:

Incentives paid in 2025 → CP58 issued by 31 March 2026.

Reporting Requirements

The form must state:

- Recipient name

- Identification number

- Total incentive amount

- Monetary and non-monetary benefits

- Company details

Accurate record-keeping is critical.

CP58 at a Glance

| Requirement | Detail |

|---|---|

| Legal Basis | Income Tax Act 1967 |

| Applies To | Agents, dealers, distributors |

| Threshold | Above RM5,000 annually |

| Issued By | Paying Company |

| Deadline | Before 31 March |

| Regulated By | LHDN Malaysia |

Where to Get the CP58 Form

Employers who need to issue CP58 can obtain the official form directly from Lembaga Hasil Dalam Negeri (LHDN).

The CP58 form is publicly available through the LHDN website and can be downloaded as a PDF.

Download the official CP58 form here:

https://phl.hasil.gov.my/pdf/pdfborang/Borang_CP58_Pin_012022_1.pdf

This form contains the required fields for reporting incentive payments, including:

- Recipient name and identification number

- Total monetary incentives

- Non-monetary benefits

- Company details issuing the statement

Employers should ensure the form is completed accurately and retained for record-keeping purposes. LHDN generally recommends that companies keep tax-related documents for at least seven years in case of audits or verification requests.

Common Employer Mistakes That Lead to CP58 Penalties (And How to Avoid Them)

Even responsible companies make CP58 mistakes — usually not because of negligence, but because of misunderstanding.

Here are the most common compliance gaps we see, especially among SMEs and growing businesses.

Mistake 1: Assuming CP58 Only Applies to Large Corporations

The CP58 obligation is based on incentive payment activity, not company size.

If your business:

- Pays commission to freelance agents

- Provides referral incentives

- Rewards distributors

- Gives performance-based bonuses outside payroll

You may fall under CP58 requirements, even if you are a small startup.

Why This Is Risky

During an audit, LHDN does not differentiate based on company size

Mistake 2: Failing to Consolidate Incentive Payments Annually

A common operational error is tracking incentive payments monthly but not aggregating them annually.

Example:

You pay RM1,000 commission monthly to an agent.

Individually, RM1,000 does not trigger attention.

But over 12 months:

RM1,000 × 12 = RM12,000

This exceeds the RM5,000 threshold.

If your accounting system does not automatically consolidate annual totals per recipient, you may unknowingly fail to issue CP58.

Why This Is Risky

Failure to issue CP58 when the threshold is exceeded may expose your company to penalties under the Income Tax Act.

Mistake 3: Confusing CP58 With EA Form

This confusion is very common among HR teams.

EA Form applies to employees under payroll.

CP58 applies to agents, dealers, and distributors who are not salaried employees.

Some companies incorrectly:

- Issue EA Form to agents

- Skip CP58 because they assume payroll reporting covers it

These are separate compliance requirements.

Why This Is Risky

Misclassification may result in:

- Incorrect tax reporting

- Payroll inconsistencies

- Audit complications

Why These Mistakes Happen

Most CP58 non-compliance is not intentional.

It usually happens because:

- There is no formal incentive tracking system

- HR and finance roles are not clearly separated

- The company is growing quickly

- There is misunderstanding about agent classification

Fixing systems early is easier than responding to audit letters later.

CP58 vs EA Form: What Employers Must Understand

| Item | CP58 | EA Form |

|---|---|---|

| For | Agents / Distributors | Employees |

| Covers | Incentives | Salary |

| Mandatory | Yes (if threshold met) | Yes |

| Issued By | Company | Employer |

Understanding the distinction prevents payroll errors and compliance exposure

Employer CP58 Compliance Checklist

Before 31 March each year, confirm:

☐ All incentive payments are recorded

☐ Total annual incentives per recipient calculated

☐ RM5,000 threshold assessed

☐ CP58 prepared accurately

☐ Copies retained for record (7 years recommended)

☐ Recipients notified

This checklist reduces audit exposure and protects your business.

Why CP58 Compliance Matters More Today

Malaysia’s tax ecosystem is increasingly data-driven.

Accurate reporting:

- Protects your company from penalties

- Supports audit readiness

- Builds professional credibility

- Strengthens governance standards

Incentive-based industries such as property, insurance, and distribution must treat CP58 as part of financial control, not optional paperwork.

FAQ

Yes, CP58 income is taxable in Malaysia.

It records commission or incentive income paid to you. Even if no tax was deducted monthly, you must declare it in your annual income tax filing.

No, they are different.

EA Form reports salary income for employees. CP58 reports commission or incentive income for agents, distributors, and commission earners. If you earn both salary and commission, you may receive both documents.

There is no fixed percentage, but a practical guideline is 20% to 30% of each commission payment.

This helps prevent cash flow stress when filing your taxes, especially in your first year.

Companies that issue CP58 report incentive payments to the tax authority.

If your declared income does not match reported data, it may trigger audit queries or additional tax assessments. It is safer to declare properly.

Yes.

Under Malaysia’s self-assessment system, all taxable income must be declared regardless of amount. Even small commission income should be included in your filing.

Running a business in Malaysia requires both compliance and strategic growth. Partner with IQI to explore investment opportunities, expand your network, and operate confidently in a transparent, regulated market.

References:

Income Tax Act 1967 (Act 53). (1967). Section 83A: Statement of monetary and non-monetary incentive payments. Government of Malaysia. https://phl.hasil.gov.my

Lembaga Hasil Dalam Negeri Malaysia. (2024). CP58 reporting guidelines and compliance requirements. https://www.hasil.gov.my

Lembaga Hasil Dalam Negeri Malaysia. (2024). Self-assessment system in Malaysia. https://www.hasil.gov.my

Continue Reading: