Version: BM

TLDR: The growing gap between unfair wages and rising living costs is causing Malaysians to struggle financially more than ever.

There’s data shared on Reddit showing that 53% of Malaysian youth have less than RM1,000 in savings.

With prices going up every year, it’s no surprise that money seems to disappear as soon as we get paid.

Whether you earn RM3,000 or RM18,000, the feeling is the same: it’s just never enough.

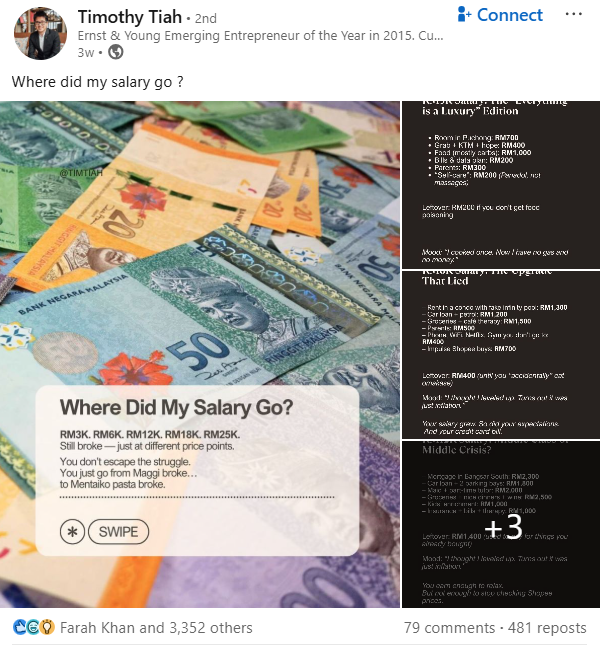

To add to that, a recent viral post on LinkedIn showing different salary tiers in Malaysia also caught people’s attention.

It shows a hard truth: even when you earn more, your expenses grow just as fast, making financial comfort feel harder to reach.

So what’s exactly happening in the salary gap in Malaysia?

Why Are We Struggling to Save?

- The Cost of “Making It” in Malaysia

- The Harsh Breakdown: Where Does the Money Go?

- Malaysia’s Wage Growth: 2020–2025

- Lifestyle Inflation: The Hidden Trap

- The Sandwich Generation Struggle

- EPF Withdrawals: A Lifeline Turned Warning Sign

- The Financial Literacy Gap

- Bridging the Gap: What Needs to Change?

- Frequently Asked Questions (FAQs)

The Cost of “Making It” in Malaysia

To understand why so many Malaysians struggle to save, we first need to look at where the money goes.

Living in urban areas like Kuala Lumpur, Selangor, Penang and Johor often comes with high fixed costs like rent, transport, food, and family obligations.

What used to be considered luxuries – café weekends, ride-hailing, gym memberships – are now part of ordinary life. But these small upgrades quietly drain disposable income.

Over time, these “little things” add up. What feels like a normal lifestyle today would have been seen as indulgent a decade ago.

Malaysians aren’t necessarily spending recklessly. They’re simply paying more to maintain the same standard of living. And that’s where the real pressure begins.

The Harsh Breakdown: Where Does the Money Go?

Ten years ago, earning RM3,000 a month was seen as comfortable. Even impressive for fresh graduates.

Today, that same figure often means living with little to no financial cushion. Many Malaysians today struggle to save even RM100 after covering monthly commitments.

A salary that once was considered decent barely covers basic needs today.

Here’s a look at a figurative breakdown of Malaysian monthly expenses across different income levels.

| Monthly Salary | Major Expenses | Leftover (if any) | Reality Check |

| RM3,000 | Room rental (RM700) Transport (RM400) Foods (RM1,000) Bills (RM200) Parents (RM300) Self-care (RM200) | ~RM200 | Every ringgit counts; basic survival, no savings |

| RM6,000 | Condo rent (RM1,300) Car + Petrol (RM1,200) Groceries (RM500) Dining out (RM500) Parents (RM500) Subscriptions (RM500) Impulse buys (RM600) Self-care (500) | ~RM400 | Slightly better comfort, but lifestyle costs inflate just as fast |

| RM18,000 | House loan (RM4,000) Car + Petrol (RM3,500) Child care (RM4,000, Families (RM3,500) Daily costs (RM3,200) | RM0–negligible | The “sandwich generation”: supporting both kids and parents leaves nothing for self |

These examples paint a consistent picture: no matter how much Malaysians earn, disposable income remains tight.

Many households, even dual-income ones, find themselves without meaningful savings or emergency funds.

Malaysia’s Wage Growth: 2020–2025

The core issue isn’t just personal spending. Over the past decade, Malaysia’s cost of living has risen much faster than wage growth.

Essentials like food, housing, and transport have outpaced salary adjustments; a reality that affects every segment of society.

According to Bank Negara Malaysia’s data, the median monthly salary for Malaysians in 2023 was around RM2,800–RM3,500, depending on sector and region.

For urban dwellers, that amount barely sustains basic living expenses, let alone savings.

When daily survival already consumes most of the income, financial planning becomes a luxury many can’t afford.

To put things into perspective, here’s how little salaries in Malaysia have changed compared to the rise in living costs.

| Year | Median Monthly Salary | Mean Monthly Salary | Year-on-Year Growth | What This Fails to Capture |

| 2022 | ~RM3,332 | — | — | After inflation, purchasing power already lower in some sectors. |

| 2023 | ~RM2,800 | ~RM3,441 | +5–7% (sector dependent) | Nominal increase, but real income decline due to inflation. |

| 2024 | RM2,793 (Median) | RM3,652 (Mean) | Median rose by ~7.3%; mean ~6.1% | Essentials: Rent, food, childcare. Rose far faster. |

| 2025 | ~RM3,045 (Formal sector Q4 2024 est.) | — | Modest increase, still below inflation | Real income stagnant; pay cheques stretched thinner. |

While wages show slight annual increases, most Malaysians don’t feel any richer. The cost of living has grown disproportionately, eroding purchasing power and leaving minimal room for savings.

Lifestyle Inflation: The Hidden Trap

Many Malaysians equate higher salaries with better lifestyles.

But the truth is, much of the “increase” goes straight into absorbing inflation.

Rent hikes, fuel prices, childcare, and food inflation have created what economists call “cost-of-living entrapment”, where higher income doesn’t translate into better quality of life.

As one viral post aptly put it: “I thought I levelled up. Turns out it was just inflation.”

The RM6K earner, for example, might move from a shared room to a condo, buy a car, or indulge in café weekends.

These upgrades, while normal, often lead to lifestyle inflation – where spending grows proportionally with income, leaving savings stagnant.

Financial experts warn that such spending patterns blur the line between “needs” and “wants.” Over time, this creates a dangerous loop: more income, more commitments, but no real financial progress.

The Sandwich Generation Struggle

For Malaysians in their 30s and 40s, being financially “comfortable” is almost impossible.

They are the sandwich generation. Supporting elderly parents while raising their own children, both financially dependent.

A combined income of RM15K–RM20K may seem substantial, but between housing loans, car payments, tuition fees, and elder care, there’s little room for savings.

As one parent summarised it online: “Every sen is spoken for. I’m just the middleman.”

This burden isn’t only emotional; it’s structural. Without robust social safety nets for retirement and healthcare, middle-income Malaysians are effectively funding three generations at once.

EPF Withdrawals: A Lifeline Turned Warning Sign

The Employees Provident Fund (EPF), or KWSP, was established to ensure Malaysians have savings for their retirement.

But in recent years, it’s increasingly been used as a short-term financial cushion.

A major change came in 2024 with the account restructuring into three parts: Akaun Persaraan, Akaun Sejahtera, and Akaun Fleksibel (Account 3).

Account 3 (Akaun Fleksibel) was introduced for members under 55 to provide flexibility.

It allows withdrawals from savings in that account for immediate and short-term needs, with minimums as low as RM50, subject to conditions.

Since its launch in May 2024, more than 4.6 million contributors – roughly 25% of EPF members under 55 – have made withdrawals, amounting to about RM14.79 billion as of mid-2025.

This shows just how many Malaysians, especially youths, are struggling to stay afloat month to month.

Many young workers find that after deductions for rent, transport, food, and family commitments, their take-home pay leaves little to nothing for savings.

When emergencies arise – from medical bills to car repairs – Account 3 becomes an easy fallback.

While this flexibility offers short-term relief, it highlights a deeper problem: Malaysians are using retirement funds to survive the present.

Every ringgit withdrawn now is a ringgit lost for the future – a small leak that could grow into a major crisis later in life.

The Financial Literacy Gap

A 2025 article by Xanderia highlighted Malaysia’s ongoing struggle with financial literacy, urging citizens to practise “5 langkah bijak” (five smart steps) to manage their money.

Despite growing awareness, poor budgeting, debt dependency, and low investment knowledge remain widespread.

Without strong literacy, even moderate-income earners find it difficult to plan ahead. Many rely heavily on credit cards, personal loans, and “buy now, pay later” schemes to fill monthly gaps.

Leading to long-term financial instability.

Bridging the Gap: What Needs to Change?

The problem isn’t just about how much people earn. It’s about the systemic imbalance between income growth, cost of living, and savings culture.

- Wages haven’t kept pace with inflation.

- Lifestyle upgrades often erase salary gains.

- Family obligations drain disposable income.

- Safety nets like EPF are being prematurely used.

- Financial literacy remains low among working adults.

The result? Even those who appear “comfortable” on paper are one emergency away from financial distress.

Malaysia’s financial reality demands both personal effort and systemic reform.

On an individual level, practising mindful spending, budgeting, and building an emergency fund are no longer optional. They’re essential for survival in today’s economy.

Financial literacy must start early, ideally in schools and through community programmes that teach young people how to manage money, understand credit, and plan for long-term goals.

But individual effort can only go so far. On a policy level, the government and employers must play their part in ensuring wage growth keeps pace with inflation.

Access to affordable housing, childcare, and public transport should no longer be viewed as privileges but as necessities that support a sustainable standard of living.

Because as seen throughout the discussion above, earning more doesn’t necessarily mean living better.

The reality for many Malaysians is that income gains are quickly swallowed by rising prices, stagnant wages, and lifestyle pressures.

Until the gap between income and sustainable living is closed, the struggle to save (and to truly thrive) will remain a shared national experience.

Frequently Asked Questions (FAQs)

1. Why are Malaysians struggling financially?

Because wages aren’t keeping up with inflation, while daily expenses continue to climb.

2. What are the most common money mistakes Malaysians make?

Overspending, lack of savings, and poor budgeting habits.

3. How can Malaysians improve their financial stability?

By practising mindful spending, saving consistently, and planning long-term finances.

4. What role does financial literacy play?

It empowers people to make smarter money decisions and avoid debt traps.

Financial struggle is real. Change your path, grow your career, and start living the life you want. Join us today.

Continue Reading: