As Bank Negara Malaysia (BNM) announced on 11 August 2021, the Standardised Base Rate (SBR) has replaced the Base Rate (BR). Since 1 August 2022, the SBR has been the main reference rate for new retail floating-rate loans and financing facilities.

This allows banks in Malaysia to determine their interest rate based on a formula set by the central bank. So how does this relate to your loan interest rate, which can vary from time to time over the lifetime of the loan?

How Does the BLR Rate Work in Malaysia?

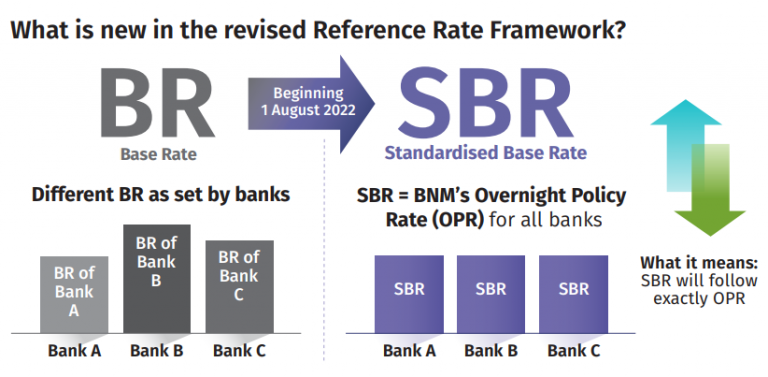

From BLR, BR to SBR

Let’s go back to the beginning. The old Base Lending Rate (BLR) was based on how much it costs to lend money to other financial institutions. Meanwhile, the cost to borrow money was determined by the central bank’s Overnight Policy Rate (OPR).

When BR was implemented in 2022, interest rates were determined by the individual banks’ benchmark cost of funds and Statutory Reserve Requirement (SRR).

How is SBR different? The main feature of the SBR is in its standardisation as the standard reference rate for all banks. Unlike the BR, which differs for each bank, the SBR is the same across banks.

Another key aspect of the SBR is that it is linked solely to the overnight policy rate (OPR). This is another simplification compared to the previous BR, which was previously determined by the banks’ individual benchmark cost of funds and the cost of holding non-interest-bearing statutory reserves with BNM.

It is important to note that the SBR is aimed at individual consumers and not SMEs.

Why the change to SBR?

According to BNM, the BR introduced in 2015 was intended to improve transparency and discipline in retail loan pricing while enhancing the transmission of monetary policy. For a time, this appeared to work well. However, since this framework allowed banks to adopt bank-specific BR methodologies that reflected their funding strategies, each bank’s BR methodologies became more complex over time.

This, in turn, reduced transparency and comparability of BRs across different banks, making things more difficult for the consumer.

As such, the SBR was introduced to promote a transparent reference rate that facilitates meaningful comparisons of loans across banks. This allows consumers to make informed decisions, reinforces sound practices in bank pricing of retail floating-rate loans, and preserves the effective transmission of monetary policy decisions.

Image source: BNM

How does the switch to SBR affect you?

The switch from BR to SBR should make it easier to understand that repayment installments will only change when there is a change in the OPR, unless there is an increase in consumer credit risk, for example, if you fail to make repayments. This means that consumers will have a more transparent picture when it comes to repaying their loans.

Additionally, since the SBR is standardised across all banks, there is no longer a need to compare differences in BR computation across banks. This makes it easier for consumers to compare their options across multiple banks.

How does it affect your loan interest rate?

For existing borrowers, the move to SBR does not affect lending rates of existing retail floating-rate loans. For new borrowers, the lending rates for retail borrowers are largely unaffected by the move to SBR. However, borrowers’ lending rates and loan repayments may still be affected by other factors, such as borrowers’ credit risk profile (e.g. repayment track record).

In order to compare interest rates across banks, you can take the following as an example:

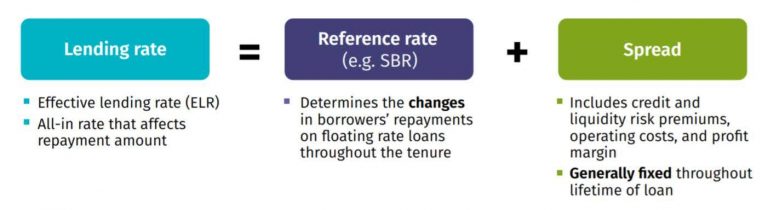

Interest rate = SBR + spread

As such:

| Interest rate on loan | SBR | Spread | |

|---|---|---|---|

| Bank A | 3.75% | 2.25% | 1.5% |

| Bank B | 4.25% | 2.25% | 2.0% |

Since SBR is now fixed across banks, differences in effective lending rates are solely driven by the spread charged by individual banks.

What is Standardised Base Rate and How is it Calculated

The Standardised Base Rate (SBR) serves as a crucial reference rate used by banks in Malaysia to price new retail floating-rate loans and financing. Unlike previous systems, the SBR is linked solely to the Overnight Policy Rate (OPR), which is determined by the Monetary Policy Committee (MPC) of Bank Negara Malaysia (BNM).

This linkage ensures a more transparent and uniform approach across all banks. To calculate the SBR, banks add a fixed margin to the OPR.

This margin is determined by each bank and is designed to cover the costs and risks associated with lending. The SBR is thus a combination of the OPR and this fixed margin, making it a straightforward and predictable reference rate.

The SBR is applied to various financial products, including new retail floating-rate loans and financing, refinancing of existing loans, and the renewal of revolving retail floating-rate loans.

However, it is important to note that the SBR is not used for pricing loans and financing for SMEs or businesses. Any changes in the OPR, whether upward or downward, will directly adjust the SBR by the same amount, ensuring consistency and transparency in loan pricing.

Factors Influencing Standardised Base Rate

Several factors influence the Standardised Base Rate (SBR), making it a dynamic reference rate that can change over time. Here are the key factors:

- Monetary Policy Committee (MPC) Decisions: The MPC sets the Overnight Policy Rate (OPR), which is the benchmark rate used to calculate the SBR. Any changes in the OPR, driven by the MPC’s decisions, will result in corresponding changes to the SBR.

- Economic Conditions: The overall economic conditions in Malaysia play a significant role in the MPC’s decisions. Factors such as inflation, economic growth, and employment rates are considered when setting the OPR, thereby influencing the SBR.

- Banking Industry Conditions: The health and stability of the banking industry also impact the SBR. Elements such as bank liquidity, credit growth, and asset quality are crucial in determining the overall lending environment, which in turn affects the SBR.

- Market Conditions: Market conditions, including prevailing interest rates and credit spreads, can influence the SBR. These conditions reflect the broader financial environment and can lead to adjustments in the reference rate.

- Regulatory Requirements: The SBR is subject to regulatory requirements set by Bank Negara Malaysia (BNM). Any changes in these regulations can impact the SBR, ensuring that it remains aligned with the broader financial and economic policies.

These factors collectively cause the SBR to fluctuate over time, impacting the interest rates charged on retail loans and financing. Understanding these influences can help borrowers anticipate changes in their loan repayments and make informed financial decisions.

What is the Effective Lending Rate (ELR)

According to BNM, the ELR is the all-in rate that affects the repayment amount. It is arrived at by adding the reference rate (like the SBR) and the bank’s spread.

The spread or range of interest that the bank charges for your loan is based on assessing your credit profile and liquidity risk, as well as the bank’s operating costs and profit margin. The chart above shows that the spread is generally fixed throughout the loan’s tenure.

Therefore, the main change to the ELR is the change in the OPR, which directly affects the SBR for floating-rate loans.

What should borrowers compare when applying for loans?

Consumers should compare the effective lending rates (ELR) before taking out a new loan to get the best deal. The ELR is the spread above the SBR quoted by different banks.

Banks usually have a product disclosure sheet (PDS) that can be easily found online. These provide key information on financial products offered by banks, including on the ELR and total repayment amount for the loan you are considering.

| Financial Institution | Base Rate (%) | Base Lending Rate (%) | Standardised Base Rate (%) | Indicative Effective Lending Rate (%) |

|---|---|---|---|---|

| Affin Bank Berhad | 3.95 | 6.81 | 3.00 | 4.55 |

| Alliance Bank Malaysia Berhad | 3.82 | 6.67 | 3.00 | 4.36 |

| AmBank (M) Berhad | 3.85 | 6.70 | 3.00 | 4.50 |

| Bangkok Bank Berhad | 4.47 | 7.12 | 3.00 | 5.67 |

| Bank of China (Malaysia) Berhad | 2.75 | 6.35 | 3.00 | 4.55 |

| CIMB Bank Berhad | 4.00 | 6.85 | 3.00 | 4.75 |

| Hong Leong Bank Malaysia Berhad | 3.88 | 6.89 | 3.00 | 4.75 |

| HSBC Bank Malaysia Berhad | 3.64 | 6.74 | 3.00 | 4.75 |

| Industrial and Commercial Bank of China (Malaysia) Berhad | 3.77 | 5.70 | 3.00 | 3.97 |

| Malayan Banking Berhad | 3.00 | 6.65 | 3.00 | 4.15 |

| OCBC Bank (Malaysia) Berhad | 3.83 | 6.76 | 3.00 | 4.70 |

| Public Bank Berhad | 3.52 | 6.72 | 3.00 | 4.35 |

| RHB Bank Berhad | 3.75 | 6.70 | 3.00 | 4.75 |

| Standard Chartered Bank Malaysia Berhad | 3.52 | 6.70 | 3.00 | 4.75 |

| United Overseas Bank (Malaysia) Bhd | 3.86 | 6.82 | 3.00 | 4.61 |

Borrowers should also understand that their monthly repayment will increase or decrease when the OPR changes. As such, they will need to plan ahead and assess whether they can continue to afford the loan repayments if the effective lending rate increases in the future.

Overall, the SBR system may actually benefit customers more in the long run. It is a more transparent reference rate, and prospective borrowers can make better financial choices when navigating an array of loan products offered by various financial institutions.

This article has been updated on January 15, 2025.

This article is a collaboration between iMoney and IQI Global. iMoney is a personal finance company that operates a comparison platform. It was founded in 2012 and has since worked with over 50 financial services partners to help build consumer financial literacy.

Connect with our professional real estate agent to help you find your dream house by submitting the form below!