Negotiator ∙ CS

Villasini Priya Raman

REN01161

Negotiator ∙ CS

Villasini Priya Raman

REN01161

About Villasini Priya Raman

Leveraging market knowledge and negotiation skills to deliver exceptional results. Your real estate success is my priority. Ready to make your real estate dreams a reality? Let's chat. Your dream home awaits.

Contact Villasini Priya Raman

Villasini Priya Raman Social Links

My Listings

No listings available at the moment.

Our newly launched projects

Discover the real estate properties in and around Kuala Lumpur, Malaysia. Buy apartment units, landed houses, bungalows, commercial office space, shop lots, and sub-sales with 100% confidence at IQI Global.

Large land area

Large land area

Northern TechValley @BKE

Mukim 14, Kubang Semang, 14400 Seberang Perai, Penang, Malaysia

Starting from RM 14,495,520

Listed on January 23, 2026

Varied built-up sizes

Varied built-up sizes

Taman IKS Bukit Minyak

Jalan IKS Bukit Minyak Utama, Taman IKS Bukit Minyak, 14100 Simpang Ampat, Penang, Malaysia.

Starting from RM 1,203,800

Listed on January 23, 2026

Industrial project type

Industrial project type

Regalway Industrial Hub (Industrial)

Regalway Industrial Hub, Off Jalan Bukit Panchor, Bukit Panchor, 14100 Simpang Ampat, Penang, Malaysia.

Starting from RM 5,015,000

Listed on January 23, 2026

Spacious land area

Spacious land area

Taman Jasa Ria (Garden Villa)

Jalan Permatang Pasir, Taman Jasa Ria, 14000 Bukit Mertajam, Penang, Malaysia

Starting from RM 1,118,800

Listed on January 23, 2026

Larger built-up area

Larger built-up area

Taman Jasa Intan (Garden Superlink)

Jalan Jasa Intan, Taman Jasa Intan, 14000 Bukit Mertajam, Penang, Malaysia

Starting from RM 818,000

Listed on January 23, 2026

Large land area

Large land area

Taman Fajar Permai (Sunrise Terrace)

Jalan Fajar, Taman Fajar Permai, 14300 Nibong Tebal, Penang, Malaysia.

Starting from RM 550,000

Listed on January 23, 2026

Mortgage Calculator

Calculate your estimated month repayment and plan your monthly expenses well.

The mortgage calculator is intended for reference only. Actual amount may vary.

Monthly Payment

Send me the mortgage calculator result

Home Loan Eligibility Calculator

Calculate your potential loan amount and assess your home buying affordability.

Rental Yield

Calculate the potential rental yield and evaluate a property's investment performance.

Down Payment Saving Plan

Create a structured savings plan and determine how much to save monthly for your down payment plan.

Malaysian Property Transaction Fees Calculator

Estimate the total transaction fees and budget accurately for your Malaysian property purchase.

IQI blog & news

Articles specifically curated for your daily digest of local and global real estate news.

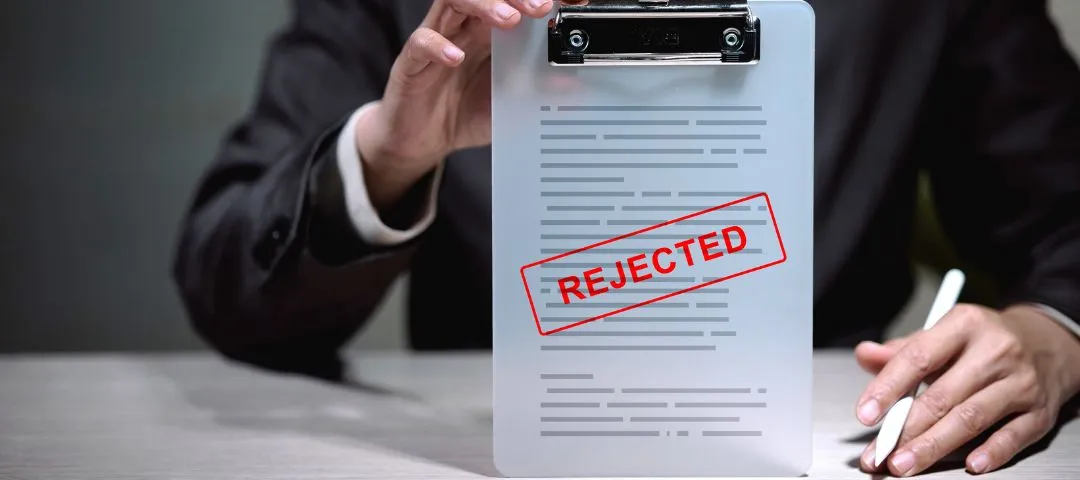

TL;DRA housing loan rejection in Malaysia often due to a high Debt Service Ratio (DSR), a poor credit history (CCRIS/CTOS), or unstable income. The key is to request feedback from your bank, check your credit reports, and then address any financial or documentation issues before reapplying after a recommended 3-6-month waiting period. That sinking feeling when your housing loan application is rejected in Malaysia? Yeah, we get it. It’s like finding the perfect durian, only for it to be snatched away at the last moment. This common scenario can leave prospective homebuyers not just disappointed, but also confused, wondering what went wrong after all the effort. Leaving these underlying issues unaddressed isn't just a missed opportunity; it can lead to repeated rejections, wasted time, and the painful experience of watching your dream property slip through your fingers. In this article, we will explain the "why" behind loan rejections in the Malaysian banking landscape, particularly its unique criteria such as Debt Service Ratio (DSR), CCRIS, and CTOS. By the end, you will be equipped with clear, actionable steps to understand your rejection, fix underlying issues, and significantly boost your chances for a successful home loan approval in Malaysia. Key Takeaway Housing loan rejections in Malaysia are usually due to issues with the financial profile. A rejection is not the end, but a signal to fix the weak points. Improving approval chances requires better debt control and stronger credit behavior. Choosing the right bank and property matters too. Your Guide to Loan Approval in Malaysia1. Top 10 Reasons Your Housing Loan Was Rejected in Malaysia2. What to Do IMMEDIATELY After Your Loan is Rejected?3. How to Improve Your Chances for Future Housing Loan Approval in Malaysia4. Frequently Asked Questions (FAQs) Estimated reading time: 23 minutes 1. Top 10 Reasons Your Housing Loan Was Rejected in Malaysia A housing loan rejected in Malaysia often stems from one or more identifiable factors, typically related to your financial standing, application accuracy, or even the property itself. Understanding these common culprits is the first step towards turning a "no" into a "yes." a. Your Debt Service Ratio (DSR) is Sky-High Debt Service Ratio (DSR) is a critical metric used by Malaysian banks to evaluate a borrower's ability to manage new debt, calculated as your total monthly debt obligations divided by your net monthly income. If your DSR exceeds the bank's maximum allowable limit, often between 50% and 70%, though it varies by bank, your housing loan application will likely be rejected. This limit ensures you have enough residual income for living expenses after servicing all your debts. i. How to Fix High Debt Service Ratio (DSR) To lower your DSR, you can either reduce your existing monthly debt commitments (e.g., credit card balances, car loans, personal loans, PTPTN loans) or increase your verifiable net income. Consider consolidating smaller unsecured loans to reduce your overall monthly outflow, or seek ways to demonstrate additional, consistent income. The DSR calculation example below illustrates how varying debt levels can impact your DSR: Salary RM5,000 = Net Income RM4,500 Salary + Rental Income RM6,000 = Net Income RM5,500 Car Loan = RM800 Personal Loan = RM200 Proposed Housing Loan = RM1,500 Formula Used DSR = Total Monthly Debt ÷ Net Income × 100 Income TypeMonthly Amount (RM)Debt TypeMonthly Payment (RM)Total Monthly Debt (RM)Net Income (RM)DSR (%)StatusSalary5,000Car Loan8008004,50017.8%HealthySalary5,000Car Loan + Personal Loan1,0001,0004,50022.2%HealthySalary5,000Car Loan + Proposed Housing Loan2,3002,3004,50051.1%BorderlineSalary5,000Car Loan + Personal Loan + Proposed Housing Loan2,5002,5004,50055.6%BorderlineSalary + Rental Income6,000Car Loan + Proposed Housing Loan2,3002,3005,50041.8%HealthySalary + Rental Income6,000Car Loan + Personal Loan + Proposed Housing Loan2,5002,5005,50045.5%HealthyAssumes new proposed housing loan payment of RM1,500 per month for illustration purposes. b. That Pesky Credit Score: CCRIS & CTOS Blacklist Banks heavily rely on your credit score, which indicates your repayment behavior and creditworthiness. A low credit score is one of the most common reasons for a housing loan rejection in Malaysia. This score is primarily derived from two key reports: CCRIS (Central Credit Reference Information System): Managed by Bank Negara Malaysia (BNM), this system records all your credit activities over the past 12 months, including housing loans, car loans, credit cards, and personal loans, and flags any irregular or late payments. Even PTPTN student loan defaults appear here. CTOS (Credit Tip-Off Service): A private credit reporting agency that compiles data from public sources, including legal notices, bankruptcy records, and trade references, offering a broader view of your financial standing. Red flags such as consistently missing due dates, high credit card utilization (maxing out credit limits), having accounts classified as "special attention accounts," or a history of bankruptcy can all lead to your housing loan application being denied. Surprisingly, having no credit history at all (a "clean CCRIS") can also be a problem, as banks have no record to assess your repayment capability. i. How to Fix Your Credit Score Obtain your latest CCRIS (via eCCRIS online or BNM kiosks) and CTOS reports to identify specific issues. Pay off outstanding debts, ensure all payments are made on time, and reduce your credit card utilization to below 30% of your limit. If you have no credit history, consider getting a basic credit card and using it responsibly for 6-12 months to build a positive record. FeatureCCRIS (Central Credit Reference Information System)CTOS (Credit Tip-Off Service)Data SourcesFinancial institutions (banks, credit card companies, development finance institutions) that report to BNM.Public records (bankruptcy notices, legal proceedings), trade references, SSM, NRIC.Key InformationLoans, credit cards, payment history for past 12 months, recent loan applications.Business background, director information, legal actions, bankruptcy status, personal credit score.Who Provides ItBank Negara Malaysia (BNM)CTOS Data Systems Sdn Bhd (private agency) c. Income Woes: Insufficient or Unstable Your income is the bedrock of your repayment capacity, and banks scrutinize it to ensure you can comfortably handle monthly mortgage repayments. If your income is deemed insufficient for the loan amount you're requesting, or if it appears unstable, your housing loan application will likely be denied. This is a common reason, as rising property prices often outpace wage growth, making it harder for many Malaysians, including middle-income buyers, to qualify. Banks prefer stable, recurring income. Freelancers or those with commission-driven jobs, for instance, may face greater scrutiny due to fluctuating earnings. i. How to make sure you have sufficient and stable income Ensure you meet the bank's minimum income requirements for the desired loan amount. If your income is variable, provide comprehensive income proof, at least 6 months of salary slips, bank statements showing consistent salary credits, and EPF contributions to demonstrate income stability. If you have other verifiable income sources, such as rental income or dividends, declare them and provide proof. d. The Dreaded Incomplete or Inaccurate Documents One of the most frustrating yet easily avoidable reasons for a housing loan rejection in Malaysia is incomplete or inaccurate documentation. Banks require extensive financial documentation to assess your eligibility, and even simple errors like incorrect addresses or contact details can lead to rejection. Crucially, banks need robust proof of income beyond just a salary voucher, often requiring salary slips, EPF contributions, savings account statements, and income tax declarations. i. How to Fix Inaccurate Documents Compile all necessary documents carefully. Use a checklist to ensure nothing is missed and that all information is accurate and up to date. Make sure copies are clear and legible. For salaried employees, a comprehensive list includes MyKad, the latest 3-6 months' payslips and bank statements showing salary credits, EPF statements (13 months), and the latest income tax papers. Self-employed individuals have a longer list, often including business registration papers, 6 months of bank statements, and latest tax returns. CategoryDocument RequiredNotesIdentity & PersonalMyKad (front and back)Clear copies.Valid Contact Details / Current AddressEnsure consistency with application form.Income Proof (Employed)Latest 3-6 months' PayslipsMust clearly show salary.Latest 3-6 months' Bank StatementsShowing salary credits.EPF Statement (latest 13 months)Proof of consistent contributions.Latest Income Tax Returns (Form BE/B)Accompanied by tax receipts.Income Proof (Self-Employed)Business Registration Papers (SSM)Valid and up-to-date.Latest 6-12 months' Company Bank StatementsReflecting business income and expenses.Latest 2 years' Audited Financial StatementsSome banks require this for larger loans.Latest Income Tax Returns (Form B)With tax receipts.Property DocumentsSale & Purchase Agreement (SPA)For sub-sale properties.Booking Form / Offer LetterFrom developer for new launches.Valuation ReportIf available, especially for sub-sale. e. Choosing the "Wrong" Bank for Your Profile It might sound odd, but sometimes a housing loan rejected in Malaysia isn't entirely about your financial health, but about the bank you applied to. Each Malaysian bank operates with its own specific set of lending policies, risk appetites, and DSR benchmarks, meaning criteria can differ significantly from one institution to another. What one bank considers high risk, another might find acceptable based on its internal credit-scoring system and preferred customer segments. This is why a rejection from one bank doesn't necessarily mean all banks will turn you down. i. How to Choose the Right Bank Don't put all your eggs in one basket, but don't apply everywhere at once either. Research the eligibility criteria and DSR limits of multiple banks before applying. Mortgage brokers can be invaluable here, as they have insight into which banks are more likely to approve your specific financial profile. Pre-assessments offered by some banks can also help gauge your chances without leaving a hard mark on your credit report. f. The Property Itself is a Red Flag Sometimes, the issue isn't you, it's the house! Banks have their own "blacklist" of properties or apply stricter criteria to certain types, leading to your housing loan application being denied. Reasons can include the property's value not matching the asking price, its legal status, or even its physical location and condition. For example, leasehold properties with less than 30 or 60 years remaining on the lease are often viewed as high risk by banks, making them difficult to finance because their value is expected to drop significantly. Properties that haven't received their strata title after many years, are located in landslide or flood-prone areas, or have bad structural integrity can also be red-flagged. Even the developer's reputation or bankruptcy status can cause issues, as banks maintain a blacklist of developers. i. How to Avoid Red-Flagged Property Perform thorough due diligence on the property and the developer before committing. Check the developer's background, including their bankruptcy status via MYEG, and look for online reviews or forum discussions. For sub-sale properties, verify the strata title status and the remaining leasehold tenure. If buying from an individual, confirm the seller is not bankrupt. FactorWhy Banks WorryWhat to CheckLeasehold TenureProperty value declines towards end of lease; high risk.Remaining lease years (many banks reject below 30-60 years).Strata Title StatusUnclear ownership, potential legal complications.Has strata title been issued? How long since completion?Developer ReputationFinancial instability, history of unfinished projects.Check MYEG for bankruptcy, online forums for reviews.Property Location/ConditionHigh-risk areas (flood, landslide), poor maintenance.Site visits, local council reports, insurance viability. g. Too Many Loan Applications In the world of credit, desperation isn't a good look. If you've been submitting multiple loan applications to various banks in a short period, this behavior is recorded on your CCRIS report as "credit inquiries". Banks interpret a high frequency of recent applications as a potential red flag, signaling that you might be desperate for credit or that other lenders have already rejected you, making them hesitant to take on the perceived risk. This can significantly lower your application score and chances of approval. i. How to Avoid Applying to Too Many Loan Applications Instead of blindly applying to every bank, strategize your approach. Use pre-assessment tools offered by banks or consult a mortgage broker to identify banks best suited to your profile. After a rejection, it's crucial to wait for a recommended period, typically 3-6 months, before reapplying. This allows you to address underlying issues and for those multiple inquiries to "cool down" on your credit report. h. Existing Commitments: High Installments or Other Loans Beyond the Debt Service Ratio, the sheer volume and type of your existing financial commitments can weigh heavily on your housing loan approval chances. Banks assess how much of your income is already tied up in other repayments, such as car loans, personal loans, or credit card bills. Even if your DSR is borderline acceptable, having numerous or high-installment unsecured loans can make a lender cautious, as it reduces your financial flexibility in the face of unexpected expenses. This concern is heightened if you have a "thick bureau" (many credit facilities) with substantial outstanding balances. i. How to manage high Commitments Prioritize paying down your highest-interest or shortest-term debts before applying for a home loan. Consider debt consolidation for unsecured loans. This can simplify your repayments and potentially reduce your overall monthly commitment, freeing up more disposable income and improving your perceived financial stability. I. Age and Loan Tenure: Are You Too Young or Too Old? Your age plays a significant, though often overlooked, role in determining your housing loan eligibility, primarily by influencing the maximum loan tenure a bank can offer. In Malaysia, loan tenures are typically capped around the borrower's retirement age, usually 65 or 70. If you're older, your shorter maximum tenure could lead to higher monthly repayments that push your DSR beyond acceptable limits, resulting in a housing loan application denied. Conversely, extremely young applicants with limited credit history or income stability might also face scrutiny. i. How to Overcome Age and Tenure If you're an older applicant, consider a shorter loan tenure if it remains affordable, or apply with a younger co-borrower or guarantor whose age allows for a longer tenure, thus reducing monthly payments. Younger applicants should focus on building a strong credit history and demonstrating consistent income over time. J. Guarantor Issues (When Your Backup Isn't Bulletproof) For some housing loan applications, especially for first-time homebuyers or those with borderline DSRs, a guarantor might be required. However, the guarantor's financial health is just as critical as the primary applicant's. If your proposed guarantor has a poor credit score, high DSR, or other existing financial commitments, their involvement can inadvertently lead to your housing loan being rejected in Malaysia. The bank sees the guarantor as a backup payer, and if the backup looks weak, the primary application suffers. i How to Choose Your Guarantor If you need a guarantor, ensure they have a strong financial profile, a healthy DSR, an excellent credit score, and a stable income. Have an honest conversation with your potential guarantor about their financial standing and the responsibilities involved before they commit. 2. What to Do IMMEDIATELY After Your Loan is Rejected? A housing loan application denied isn't the end of the world; it's a signal that something needs attention. The smartest first move is to plan, not to panic. These four steps will help you understand why your home loan was rejected in Malaysia and set you on the right path. a. Request a Rejection Reason from the Bank Your first immediate step should be to contact the bank that rejected your application and politely request the reason for their decision. While banks may not always provide detailed explanations due to internal policies, they often offer general feedback such as "insufficient income," "high existing debt," or "adverse credit record." Even vague reasons can confirm your suspicions and help you focus your efforts. Understanding the specific "why" is crucial for a targeted fix, rather than guessing what went wrong. b. Get Your CCRIS and CTOS Reports (Your Financial Report Card) Before doing anything else, obtain and review your latest CCRIS and CTOS reports. These reports are your financial report card, revealing exactly what banks saw when they assessed your application. How to get your CCRIS report: Visit a Bank Negara Malaysia (BNM) kiosk with your MyKad, or register for eCCRIS online via the BNM website. How to get your CTOS report: Visit the CTOS website or use their app to sign up and view your MyCTOS Score Report, which includes both your CTOS Score and CCRIS records. Look for missed payments, high outstanding balances, signs of identity theft, or any inaccurate information that could be hurting your score. Dispute any errors immediately. c. Review Your Documents for Errors Sometimes the simplest mistakes are the most costly. After a rejection, re-examine every document you submitted for accuracy and completeness. A missing salary slip, an outdated bank statement, or even a typo in your contact details can be enough to trigger an automatic rejection. Ensure that your proof of income aligns perfectly with what's declared and that all copies are clear and legible. A second pair of eyes on your application can often catch overlooked errors. d. Don't Reapply Immediately It's tempting to immediately apply to another bank after a housing loan is rejected in Malaysia, but resist the urge. Multiple credit inquiries in a short period are recorded on your CCRIS report and can make you appear desperate, further diminishing your chances. Instead, wait for the recommended 3-6 months before submitting a new application. This crucial waiting period allows you time to address any identified issues from your credit reports or financial profile, and for the previous inquiries to "cool down". 3. How to Improve Your Chances for Future Housing Loan Approval in Malaysia After understanding why your home loan was rejected in Malaysia, the next phase is to take actionable steps for improvement. This comeback plan focuses on strengthening your financial profile and application strategy to significantly boost your approval odds. a. Master Your DSR: Reduce Debt, Boost Income To overcome a high Debt Service Ratio (DSR), focus on two core strategies: aggressive debt reduction and income enhancement. Prioritize paying down high-interest debts, such as credit card balances or personal loans, which can drastically reduce your monthly commitments and free up more disposable income. Consider debt consolidation for unsecured loans. Simultaneously, explore ways to increase your verifiable income, whether through a promotion, a side hustle, or by ensuring all legitimate income sources (e.g., rental income with valid tenancy agreements) are documented thoroughly. b. Polish Your Credit Score: The Road to Financial Gold A stellar credit score is your golden ticket. The best way to polish it is through consistent, timely payments on all your existing debts. Ensure you never miss a due date for any loan or credit card for at least 6-12 months. Reduce your credit card utilization to well below 30% of your limit, as maxing out cards indicates financial stress. If you have a "clean" CCRIS (no credit history), start by getting a basic or secured credit card, using it for small purchases, and paying it off in full each month to build a positive payment history. c. Get Your Documents in Order A well-organized and accurate set of documents can make or break your application. Create a comprehensive "pro-level checklist" and keep all financial records meticulously organized. This includes: MyKad (clear copies). Latest 6 months' payslips and bank statements (showing salary credits). Latest EPF statement (at least 13 months). Latest income tax returns (Form BE/B) with payment receipts. Any additional income proofs (e.g., valid tenancy agreements for rental income). Property documents (SPA, booking forms). Ensure all information is consistent across documents and matches your application form. d. Seek Professional Guidance Navigating the varied criteria of Malaysian banks can be daunting. Mortgage brokers are invaluable allies who can significantly improve your chances. They understand the different risk appetites and lending policies of various banks, allowing them to match your specific financial profile with the most suitable lender. A good broker can also advise you on how to best present your application and which aspects of your financial profile need the most attention. This targeted approach minimizes the risk of another housing loan being rejected in Malaysia due to applying to the wrong institution. e. Explore Government Schemes (Especially for First-Time Homebuyers) First-time homebuyers in Malaysia may find additional avenues for approval through government-backed housing schemes. Programs like the "My First Home Scheme" (Skim Rumah Pertamaku) or other initiatives from institutions like BNM aim to help eligible individuals secure financing by offering higher financing margins or specific criteria. While the specific terms and eligibility vary, exploring these options could provide alternative paths to homeownership if traditional bank loans prove challenging. f. Consider a Stronger Guarantor (If Necessary) If your application is still struggling and a guarantor is a viable option, carefully consider whom you choose. A strong guarantor can significantly bolster your application. They should ideally have a stable, high income, a low DSR, and an excellent credit score. Their financial health directly impacts the bank's assessment of your combined repayment capability, making it easier for the bank to approve the loan. Ensure the guarantor fully understands their financial commitment and responsibilities. g. Property Due Diligence: Research, Research, Research! Don't let your dream home become your biggest headache. Comprehensive property due diligence is crucial. Research the developer's track record, check for any past issues or blacklistings, and verify the property's legal status, especially its leasehold tenure and strata title. Ensure the property's valuation aligns with the asking price and that there are no hidden structural or location-based issues. Being proactive here can prevent a housing loan rejection in Malaysia due to property-related red flags. Receiving a housing loan rejection in Malaysia can feel like a roadblock on your journey to homeownership, but it's crucial to remember it's often just a detour, not a dead end. By understanding the common reasons behind these rejections, from DSR woes and credit score hiccups to documentation missteps and property-specific concerns, you gain the power to turn the situation around. With patience, careful preparation, and a strategic approach to improving your financial profile, your dream home is well within reach. Don't let a "no" discourage you; use it as motivation for a smarter, more successful reapplication. 4. Frequently Asked Questions (FAQs) a. What is a good DSR to avoid housing loan rejection in Malaysia? A good Debt Service Ratio (DSR) to aim for in Malaysia is typically between 50% and 60% to maximize your chances of loan approval, although some banks may accept up to 70% depending on factors such as income level and age. The ideal range ensures that a significant portion of your net income remains available after all debt repayments, making you a less risky borrower. It’s important to remember that DSR limits can vary from bank to bank. b. Can a low credit score cause a housing loan to be rejected in Malaysia? Yes, a low credit score is one of the most common reasons for housing loan rejection in Malaysia. Banks use credit reports like CCRIS and CTOS to assess your repayment behavior and creditworthiness. Factors such as late or missed payments, high credit card utilization, and bankruptcy records significantly lower your score, signaling a higher risk of default to lenders. Even a lack of any credit history can be viewed negatively by some banks. c. How can I check why my home loan was rejected in Malaysia? To find out why your home loan was rejected in Malaysia, first contact the bank directly and politely request the specific reason for the decision. Simultaneously, obtain your latest CCRIS report from Bank Negara Malaysia (via eCCRIS online or kiosk) and your MyCTOS Score Report from CTOS. These reports will reveal your credit history, existing debts, and any past rejections, helping you pinpoint the exact issues. d. Do banks in Malaysia reject loans due to unstable employment? Yes, banks in Malaysia can and often do reject loans due to unstable employment, as they prioritize stable, verifiable income. Inconsistent income from commission-based jobs or a short employment history can raise concerns about your long-term ability to meet monthly mortgage payments. Providing comprehensive documentation, like 6-12 months of salary slips, bank statements, and EPF contributions, helps demonstrate income stability. e. How long does it take to reapply for a housing loan after rejection in Malaysia? It is generally recommended to wait 3 to 6 months before reapplying for a housing loan after a rejection in Malaysia. This period allows you to identify and fix the issues that led to the initial rejection, such as improving your credit score or reducing debt. It also ensures that multiple credit inquiries in a short timeframe do not further negatively impact your credit profile. f. Is it possible to appeal a rejected housing loan in Malaysia? While there isn't a formal, universal "appeal process" across all Malaysian banks, as there is for legal decisions, you can certainly re-engage with the bank after a rejection. This involves understanding the specific reason for denial, addressing those issues (e.g., improving DSR, clearing credit black marks), and then resubmitting a stronger application or providing additional supporting documents. It's more of a reapplication with corrected information rather than a formal appeal. g. What role does CTOS play in housing loan rejections in Malaysia? CTOS (Credit Tip-Off Service) plays a significant role in housing loan rejections in Malaysia by providing banks with a comprehensive view of applicants' financial backgrounds. Beyond CCRIS data, CTOS reports also include information from public records such as bankruptcy notices, legal actions, and business registrations. A poor CTOS Score or adverse records (e.g., litigation, bankruptcy) can significantly impact a bank's assessment of your creditworthiness, making them cautious about approving new loans. Don't let a rejected housing loan keep you from your dream. Take control of your housing future and get personalized advice from IQI Global today! [custom_blog_form] Continue Reading Malaysia vs Singapore Property: Why Investors Still Choose KL? Where Should You Retire in Malaysia? Best Affordable, Quiet and Safe Homes to Consider 7 High Rental Potential Properties in Kepong Investors Should Watch in 2026 References Bank Negara Malaysia (BNM). (2017, July 18). Access to financing is not the primary issue for affordable housing. Retrieved from https://www.bnm.gov.my/-/access-to-financing-is-not-the-primary-issue-for-affordable-housing Berinda Properties. (2024, July 30). What Are Your Options After Your Home Loan Application Is Denied?. Retrieved from https://www.berinda.com/what-are-your-options-after-your-home-loan-application-is-denied/ Chandra, C.. (2025, December 2). Why Was Your Loan Or Credit Card Application Rejected?. RinggitPlus. Retrieved from https://ringgitplus.com/en/blog/the-experts-corner/why-was-your-loan-or-credit-card-application-is-rejected.html Chua, G.. (2022, February 28). Top 10 Reasons Your Home Loan Application Was Rejected In Malaysia. PropertyGuru. Retrieved from https://www.propertyguru.com.my/property-guides/top-10-reasons-on-why-your-loan-application-maybe-declined-3795 CTOS. (2026, April 9). Why Your Loan Got Rejected in Malaysia — and What to Check First. Retrieved from https://ctoscredit.com.my/learn/why-your-loan-got-rejected-in-malaysia-and-what-to-check-first/?srsltid=AfmBOop3MYF-i8Vi173oXGzZ9jGObMUo2UiKWxd906eu1VxnKBuH0hw1 FORTUNE. (n.d.). Top reasons why some homes in Malaysia can’t get a loan. Retrieved from https://www.fortune.my/top-reasons-why-some-homes-in-malaysia-cant-get-a-loan.htm Hariri, A.. (2025, March 24). Can’t Get a Loan? Check If You’re Blacklisted by Banks in Malaysia. PEPS Ventures Learning Resources. Retrieved from https://resources.pepsventures.com/cant-get-loan-how-to-check-if-youre-blacklisted-by-banks-malaysia iproperty. (2024, June 26). What can you do after your home loan gets rejected?. Retrieved from https://www.iproperty.com.my/guides/what-can-you-do-after-your-home-loan-gets-rejected-loancare-27923 Khoo, N.. (2017, December 29). Property: Seven reasons your loan application gets rejected. The Edge Malaysia. Retrieved from https://theedgemalaysia.com/article/property-seven-reasons-your-loan-application-gets-rejected Lekham, D.. (2026, March 13). Tightening financing, loan rejections derail home purchases in Malaysia. NST. Retrieved from https://www.nst.com.my/property/2026/03/1396266/tightening-financing-loan-rejections-derail-home-purchases-malaysia Maybank. (2019, August 21). Home Financing Rejection. Retrieved from https://www.maybank2own.com/portal/news?item_id=20 propertyguru. (2022, February 20). Bank Loan Execs Share Why Home Loan Applications Are Rejected. Retrieved from https://www.propertyguru.com.my/property-guides/why-are-home-loan-applications-rejected-malaysia-15953 Yeoh, M.. (2022, October 19). Who do we blame when our home loan gets rejected?. iproperty. Retrieved from https://www.iproperty.com.my/guides/who-do-we-blame-when-our-home-loan-gets-rejected-ctr-28464 Yeoh, M.. (2024, December 10). 9 Reasons Why Banks Reject Your Home Loan Application. iproperty. Retrieved from https://www.iproperty.com.my/guides/home-loan-rejection-reasons-41476

3 Jun, 2026

Discover Melaka's 7 Most Richest Neighborhoods: Where Malaysia's Historic Charm Meets Modern Luxury

Melaka often gets overshadowed in Malaysia's property conversation. People fixate on Kuala Lumpur's glitz, Selangor's family appeal, or Penang's island charm. Meanwhile, Melaka quietly evolves into something genuinely special: a state where heritage sophistication meets contemporary luxury. Here's what's interesting about Melaka's property market. You get historic charm that money can't replicate. UNESCO heritage surroundings. A lifestyle that balances prestige with authenticity. Plus, property values here tell a different story than KL or Selangor. They're appreciating steadily because demand is real, not speculative. This guide explores seven neighborhoods where Melaka's elite choose to establish their homes. Each neighborhood tells distinct stories about what success looks like in Malaysia's most historically significant state. Whether you're a heritage enthusiast seeking timeless elegance, a family prioritizing space and safety, or an investor recognizing Melaka's emerging opportunities, this guide reveals where the real Melaka story is being written.Melaka often gets overshadowed in Malaysia's property conversation. People fixate on Kuala Lumpur's glitz, Selangor's family appeal, or Penang's island charm. Meanwhile, Melaka quietly evolves into something genuinely special: a state where heritage sophistication meets contemporary luxury. Here's what's interesting about Melaka's property market. You get historic charm that money can't replicate. UNESCO heritage surroundings. A lifestyle that balances prestige with authenticity. Plus, property values here tell a different story than KL or Selangor. They're appreciating steadily because demand is real, not speculative. This guide explores seven neighborhoods where Melaka's elite choose to establish their homes. Each neighborhood tells distinct stories about what success looks like in Malaysia's most historically significant state. Whether you're a heritage enthusiast seeking timeless elegance, a family prioritizing space and safety, or an investor recognizing Melaka's emerging opportunities, this guide reveals where the real Melaka story is being written. 1. Heeren Street, Jalan Tun Tan Cheng Lock: The Ultimate Heritage Prestige Price Range: RM3,000,000 – RM23,000,000+ (Source: CNA Luxury, Tatler Asia) The Story Behind the Address Heeren Street isn't just a location. It's Malaysia's most historically significant millionaires' row. Positioned in Melaka's UNESCO heritage core, along Jalan Tun Tan Cheng Lock, these properties represent genuine "Crazy Rich Asians" territory – not movie fiction, but documented Melaka reality. Properties here appreciate fundamentally differently than anywhere else in Malaysia. They're not just residences. They're cultural heritage investments. Many families have held these addresses for generations, creating intergenerational wealth markers. Who Lives Here Successful business magnates. Established heritage collectors. Families with deep Melaka roots and contemporary wealth. International buyers recognizing Malaysia's cultural significance. These aren't first-time property buyers. These are people who've already built substantial success elsewhere and chosen Heeren Street as their prestige statement. The Heritage Premium What makes Heeren Street genuinely exclusive? The properties themselves. Heritage Private Villas (conservation-status renovated ancestral homes) and Mansions (exclusive ultra-premium homes) command appreciation precisely because they're irreplaceable. You can't build "heritage" overnight. These addresses took centuries to accumulate their significance. Nearby Lifestyle Elements Jonker Walk – The bustling night market experience Heeren Mansion – Architectural heritage preserved The Stadhuys – Dutch colonial heritage Traditional Chinese shophouses – Living heritage commerce Investment Perspective Heeren Street properties appreciate through scarcity + heritage premium + intergenerational desirability. Unlike typical real estate, these properties become more valuable as modernization makes heritage increasingly scarce. 2. Straits Courtyard / Kota Laksamana: The Modern Prestige Statement Price Range: RM3,500,000 – RM5,000,000+ (Source: Property Guru, IQI Global) Melaka's Premier Modern Luxury While Heeren Street celebrates heritage, Straits Courtyard represents Melaka's answer to "Malacca's Most Premier Living" – contemporary luxury without apology. This gated community adopts breakthrough anti-climb security technology. Every three-storey bungalow features private elevators and rooftop gardens. The positioning targets new-generation Melaka wealth: entrepreneurs, corporate executives, and international professionals seeking modern amenities merged with Melaka's sophisticated environment. The Security & Privacy Appeal What differentiates Straits Courtyard fundamentally? Advanced security systems. Private access. Ultra-low density planning. This appeals to successful entrepreneurs and business owners prioritizing both prestige and genuine privacy. Community Character Straits Courtyard residents are predominantly new-money Melaka professionals. Business owners. Corporate leaders. People building contemporary success and wanting appropriate environment reflection. The community is intentionally exclusive – selective entry, vetted residents, curated lifestyle. Surrounding Amenities One Street Food Row – Trendy dining district Encore Melaka – Shopping entertainment Jonker Street – Night market vibrancy Melaka waterfront – Emerging development Investment Appeal Newer properties typically appreciate slower than established neighborhoods. However, Straits Courtyard's ultra-premium positioning, limited inventory, and Melaka's growing international recognition create steady appreciation. This suits long-term investors prioritizing stability over spectacular returns. 3. 8 Residence, Padang Temu / Ujong Pasir: The Emerging Cosmopolitan District Price Range: RM1,988,000 – RM4,300,000+ (Source: PropertyGuru, PB Realty Brochure) Melaka's Answer to Waterfront Living 8 Residence represents something genuinely new for Melaka: integrated waterfront development combining heritage conservation with contemporary residential. The "8" symbolizes auspicious positioning. The gated, fully-enclosed security concept appeals to those wanting prestige community without compromise. The Unique Positioning What makes 8 Residence distinctive? They've mastered something difficult: modern development respecting heritage context. Three-storey standalone villas positioned along waterfront, with comprehensive planning prioritizing environmental quality and community integration. The development specifically targets middle-to-upper income professionals and families appreciating Melaka's lifestyle advantages without sacrificing modern convenience. Waterfront Appeal Padang Temu location provides genuine waterfront access. Not "near water," but integrated water-oriented living. Maritime heritage surrounds the development. Residents enjoy authentic Melaka waterfront experience while maintaining contemporary comfort standards. Nearby Attractions Ikan Bakar Alai – Waterfront dining culture Portuguese Settlement – Heritage village experience Dataran Pahlawan – Shopping complex Melaka waterfront – Evening promenade lifestyle Investment Perspective 8 Residence appeals to middle-to-upper income buyers seeking balance: prestige + affordability + lifestyle. As Melaka's waterfront develops further, these properties appreciate through infrastructure improvement and growing international tourism interest. 4. Ayer Keroh: The Forest-Retreat Luxury Address Price Range: RM1,200,000 – RM3,500,000+ (Source: NuProp, IQI Global) Melaka's Premier Hill Resort Living Ayer Keroh operates completely differently from urban neighborhoods. Positioned as Melaka's government administrative center, this hillside community attracts government officials, high-ranking professionals, and those prioritizing tranquil lifestyle over urban intensity. Ozana Impian Resort represents the signature development – exclusive positioning targeting those valuing low-density living and golf course proximity. Properties here emphasize environmental quality: greenification, multiple golf courses, privacy through natural terrain. The Administrative Prestige What's genuinely interesting? Ayer Keroh attracts a specific demographic: government leaders, successful professionals, those building legacies in professional institutions. The neighborhood reflects administrative prestige without commercial intensity. Lifestyle Philosophy Ayer Keroh residents prioritize space, privacy, and environmental quality. Many maintain gardens, appreciate nature, value tranquility. This creates different community character than urban neighborhoods – more conservative, professionally-focused, family-oriented. Surrounding Amenities Tiara Melaka Golf Club – Championship golf facilities MITC Melaka – International trade center AEON Ayer Keroh – Retail shopping Melaka International Trade Center – Business proximity Investment Profile Ayer Keroh appreciates through infrastructure development and growing administrative investment. Unlike speculative plays, these properties appeal to conservative investors prioritizing stability and lifestyle quality. 5. Klebang: The Coastal Getaway Prestige Price Range: RM1,000,000 – RM2,800,000+ (Source: PropertyGuru, IQI Global) Melaka's Golden Coastline Living Klebang represents something increasingly valuable: genuine beach living in Malaysia's most heritage-conscious state. This coastal neighborhood attracts international buyers, holiday home seekers, and those valuing beach lifestyle authenticity. The positioning as "Johor Pearl" of Melaka is apt. Properties command genuine waterfront appeal – direct beach access, maritime culture, authentic fishing village atmosphere alongside contemporary residential development. The Beach Community Distinction What differentiates Klebang? Authenticity. This isn't manufactured beach resort. This's actual coastal community where maritime culture remains integrated into daily life. Residents coexist with fishing heritage, traditional boat culture, genuine seaside living. Vacation Home Appeal Klebang attracts two demographics: primary residents wanting beach lifestyle, and vacation home investors recognizing rental income potential. The development sits perfectly for weekend escape from Kuala Lumpur while maintaining prestige residential standards. Nearby Attractions Klebang Coconut Shake – Iconic local experience Submarine Museum – Unique cultural attraction Local fishing village – Authentic maritime culture Melaka waterfront – Developing tourism infrastructure Investment Consideration Klebang appreciates through tourism development and international buyer interest. Properties here perform well in vacation rental market, supporting investment viability alongside lifestyle appeal. 6. Taman Bukit Cheng: The Commercial Prestige Hub Price Range: RM395,000 – RM2,000,000+ (Source: IQI Global, PropertyGuru) Melaka's Business Excellence District Taman Bukit Cheng occupies unique positioning: not residential-only, but commercial-residential integration. Located on hillside (Bukit Cheng), this neighborhood represents "hidden wealth" district – successful business owners clustering in areas prioritizing convenience over flashiness. The nickname "Taman Cheng Utama" reflects this positioning. Properties feature "large land, high usability" positioning – appealing to those building home offices, professional operations, or combining residential prestige with commercial practicality. The Business Owner Appeal Residents here are predominantly entrepreneurs, corporate leaders, those operating sophisticated business operations from home-office environments. The neighborhood reflects practical success rather than ostentatious wealth display. Neighborhood Character Taman Bukit Cheng maintains more conservative, business-focused atmosphere than other Melaka neighborhoods. Communities tend toward professional networks, business relationships, economic pragmatism. This creates different social dynamic than purely residential areas. Surrounding Business Infrastructure Lotus's Cheng – Commercial hub McDonald's DT – Regional facility Malim Business Park – Commercial development Multiple commercial centers – Supporting infrastructure Investment Profile Taman Bukit Cheng appreciates through practical value rather than speculative appeal. Business owners recognize strategic positioning, comprehensive amenities, and location convenience. Properties maintain steady appreciation driven by fundamental demand rather than market trends. 7. Bemban Country Villas Resort: The Emerging Luxury Escape Price Range: RM700,000 – RM1,500,000+ (Source: iHousing, PropertyGuru) Melaka's Newest Prestige Development Bemban represents something genuinely new: high-end country living integrated with resort amenities. Positioned on former agricultural land, with Parkland Avenue developments and hot spring resort integration, this neighborhood attracts those seeking "big space, slow life" philosophy. This development specifically targets successful professionals recognizing that Melaka's emerging prestige provides opportunity for premium country living at prices significantly more accessible than KL or Penang equivalents. The Resort-Lifestyle Integration What's genuinely innovative? Bemban merges residential prestige with resort experience. Residents access hot spring facilities, integrated recreation, and hotel-quality amenities from primary residence – creating unique lifestyle proposition in Malaysian market. The Space Philosophy Bemban explicitly markets around "Land Size" proposition. In Melaka, you can purchase substantial acreage at prices making genuine country estate living accessible. This appeals fundamentally to those wanting genuine space without resort-only visiting. Nearby Attractions Jasin Hot Spring – Integrated wellness facilities Mydin Jasin – Shopping convenience Bemban countryside – Peaceful rural character Emerging resort infrastructure – Lifestyle amenities Investment Appeal Bemban appreciates through emerging development positioning. As Melaka's resort and wellness tourism develops, these properties appreciate through both residential appreciation and tourism-related infrastructure growth. Understanding Melaka's Property Market Dynamics What Makes Melaka Different Melaka's market differs fundamentally from other Malaysian states. This isn't speculation-driven. It's heritage-premium driven. Properties appreciate through: Historical Significance - UNESCO heritage creates permanent value premium Authenticity - Genuine lifestyle cannot be replicated elsewhere International Recognition - Growing tourism and expatriate interest Space Availability - Melaka still offers space advantages over KL/Selangor Heritage Preservation - Conservation requirements protect neighborhood quality Investment Mentality Differences Melaka investors think differently than KL or Selangor buyers. This isn't "flip quickly for profit" market. This's "establish legacy, enjoy lifestyle, appreciate steadily" market. Properties here attract: Heritage enthusiasts valuing authenticity Families seeking balanced lifestyle Business owners wanting prestige addresses International buyers recognizing Malaysia's cultural importance Long-term investors prioritizing stability Market Maturity Perspective Unlike KL's saturated market or Penang's competitive island positioning, Melaka remains relatively underdeveloped in premium property conversation. Early positioning in well-selected neighborhoods offers genuine opportunity. Comparative Analysis: Finding Your Melaka Neighborhood CategoryLocationWhy?Heritage & Prestige CombinedHeeren StreetIrreplaceable historical significance, intergenerational wealth positioning, genuine "Crazy Rich Asians" authenticity, heritage premium appreciation.Modern Luxury Without CompromiseStraits CourtyardIntegrated waterfront access, heritage respect, gated security, emerging cosmopolitan lifestyle.Waterfront Living with Heritage Context8 ResidenceIntegrated waterfront access, heritage respect, gated security, emerging cosmopolitan lifestyle.Forest-Retreat TranquilityAyer KerohGolf course integration, low-density development, administrative prestige, environmental quality prioritization.Beach Lifestyle with Investment PotentialKlebangGenuine beach access, authentic maritime culture, vacation rental income potential, international appeal.Business Owner PracticalityTaman Bukit ChengCommercial-residential integration, professional networking, practical amenities, strategic business location.Emerging Country Living PrestigeBembanResort-integrated amenities, substantial land access, wellness facilities, emerging development positioning. Melaka vs. Other Malaysian States: Strategic Positioning Melaka vs. Kuala Lumpur KL Advantages: Commercial intensity, cosmopolitan diversity, rapid development Melaka Advantages: Heritage authenticity, space, prestige without density, lifestyle quality Melaka vs. Selangor Selangor Advantages: Family volume market, education infrastructure, employment density Melaka Advantages: Sophistication without suburban sprawl, heritage premium, property appreciation through scarcity Melaka vs. Penang Penang Advantages: Island prestige, established international reputation, tourism maturity Melaka Advantages: Lower pricing, growth potential recognition, less saturated market, authentic heritage without tourist overwhelm The Johor Connection Already explored Johor's property opportunities? Discover Johor's 7 most richest neighborhoods and understand how Melaka and Johor offer different value propositions for different investor profiles. Johor emphasizes space and Singapore proximity. Melaka emphasizes heritage authenticity and international prestige. Both offer genuine Malaysian opportunities beyond KL saturation. The Honest Property Investment Perspective What Melaka Offers Genuinely Melaka works exceptionally well for specific profiles: Heritage enthusiasts get authentic preservation without artificial resort atmosphere Family-focused buyers find space and safety with sophisticated cultural context Business owners establish prestigious addresses supporting professional credibility International investors recognize Malaysia's cultural significance materializing in property value Long-term thinkers understand heritage appreciation as permanent wealth vehicle What Melaka Doesn't Offer Melaka isn't for those seeking: Pure commercial intensity (that's KL) Island prestige (that's Penang) Suburban family convenience (that's Selangor) Speculative quick appreciation (that's not Melaka's market) Market Development Trajectory Melaka property market is evolving thoughtfully: Infrastructure Development: Improved highway connectivity, airport expansion, commercial center growth Tourism Investment: Growing international recognition, resort development, cultural tourism International Interest: Increasing expatriate communities, international buyer awareness Heritage Preservation: Conservation efforts protecting neighborhood quality Commercial Integration: Balanced development supporting both lifestyle and investment Early positioning in well-selected neighborhoods offers appreciation potential while Melaka's international recognition builds. Do You Think You Live in an Expensive Neighborhood? Here's the real question worth honest consideration. Among Melaka's seven premium neighborhoods, which resonates most with your actual values? Not your aspirations. Not what sounds impressive. Your genuine values. Does Heeren Street's heritage authenticity call to you? Does Straits Courtyard's contemporary prestige appeal? Does Bemban's space philosophy align with your actual lifestyle preferences? The most successful real estate decisions aren't about choosing the "most expensive" address. They're about selecting the neighborhood that genuinely reflects who you are and how you want to live. Some people find prestige in historic preservation (Heeren Street speaks to them). Others in contemporary luxury (Straits Courtyard resonates). Still others in coastal authenticity (Klebang calls to them). So here's the honest closing question: Among Melaka's expensive neighborhoods, which one actually represents your definition of an expensive, prestigious, genuine home? The answer reveals not just your property preferences, but your actual priorities in life. Ready to Explore Melaka's Premium Neighborhoods? IQI Global understands Melaka's market deeply. We're not just property agents – we're neighborhood guides. We understand heritage significance, investment trajectories, community cultures, and lifestyle implications. Let us help you by you submitting your details below! [custom_blog_form] Continue reading: Discover Penang’s 7 Most Richest Neighborhoods: The Pearl of Malaysia’s Luxury Living Beyond Kuala Lumpur: Discover Selangor’s 8 Most Richest Neighborhoods Why Melaka Is the Best Place for an Affordable House? Explore Top 7 States for Property Investment in Malaysia! Melaka Property Insights: Is Now the Perfect Time to Invest?

TL;DR A career reset at 25 is not failure. For many Gen Z Malaysians, real estate is becoming a serious career path because it offers flexibility, performance-based income, personal branding opportunities, and the chance to build long-term financial growth beyond a fixed 9-to-5 job. You graduated, landed what everyone called a “decent” job, and six months later, you’re already searching for “how to resign without ruining my career.” Sound familiar? For many Gen Z Malaysians, being 25 today feels very different from what they were promised. A stable 9-to-5 may offer security, but it does not always offer growth, purpose, flexibility or enough income to keep up with real life. That is why a career reset is no longer seen as failure. For a growing number of young Malaysians, it is a smart pivot. And with real estate offering performance-based income, personal branding opportunities and greater control over how they work, property is becoming one of the most serious career options on the table. Key Takeaways A career reset at 25 is not failure. For many Gen Z Malaysians, it is a practical response to rigid jobs, slow salary growth, burnout, and changing career expectations. Real estate is becoming a serious career option for Gen Z. It offers flexibility, performance-based income, personal branding opportunities, and a faster entry path compared to many traditional professions. Becoming a property agent in Malaysia is more accessible than many young people think. With the right certification, agency support, and REN registration process, Gen Z can start building a real estate career without needing years of additional study. Gen Z agents have a strong digital advantage. Their ability to use social media, short-form videos, personal branding, and online communication helps them build trust and attract property leads in a modern market. The right agency can make or break a young agent’s growth. Training, mentorship, technology, culture, and proven support systems are key for Gen Z Malaysians who want to succeed in real estate. From Burnt Out to Booked OutWhy Gen Z is done with the traditional 9-to-5 scriptWhy Real Estate Makes Sense for a Career ResetHow to Become a Property Agent in Malaysia (Step-by-Step)The Gen Z Advantage: Why Young Agents Win in Today's MarketWhat to Look for in a Real Estate Agency as a Young AgentIs Real Estate Your Next Career Move? Why Gen Z is done with the traditional 9-to-5 script Let’s be honest. The traditional career path was not built for how Gen Z thinks, works or lives today. Many Gen Z workers are already thinking about switching jobs. Some expect to change careers several times throughout their working lives, while others plan to leave their current employer before reaching the two-year mark. This does not mean they cannot commit. It means they are no longer willing to settle for a career that offers little growth, limited flexibility and slow income progress. In Malaysia, this shift is becoming more visible. Many young workers are leaving their jobs as early as 18 months in, not because they are lazy, but because the gap between what they were promised and what they actually experience is becoming too wide to ignore. For many, the reality of work does not match their expectations around salary, career growth, work-life balance and personal fulfilment. The real issue is that the traditional employment model was designed for a different era. Clock in, work hard, wait for a promotion and repeat the same cycle for decades. That deal made sense when loyalty was clearly rewarded. Today, many young Malaysians are questioning whether that path still leads to the future they want. Gen Z did not break the career system. They simply stopped pretending it was still working for everyone. A career reset is not giving up. It is growing up. Why Real Estate Makes Sense for a Career Reset Most people assume a career change means going back to school, accepting a lower salary or spending years starting over from zero. Real estate works differently, and that is exactly why it is becoming a serious career option for many young Malaysians. Here’s what makes a real estate career stand out: No salary ceiling. Your income is tied to your performance, not your job grade. Close more deals, earn more money. It's that direct. Curious about the real numbers? Here's an honest breakdown of what property agents actually earn in Malaysia. You own your schedule. Real estate rewards discipline and drive, not hours spent warming a chair. If you're the type who works better with autonomy, this career is built for you. Low barrier to entry. You don't need a degree, years of experience, or a fancy resume. What you need is the right certification, the right agency, and the right attitude. You're always learning about wealth. Every day in real estate is a masterclass in property, investment, negotiation, and market trends. That knowledge doesn't just make you a better agent but also makes you a smarter person financially. In fact, Gen Z and Millennials are already rewriting the wealth playbook, and real estate is right at the centre of it. Gen Z Malaysians are also becoming more active in the property market as buyers and renters themselves. This gives young agents a valuable advantage. They understand what today’s buyers worry about, what they look for online and what kind of communication feels trustworthy. For a generation that values growth, freedom and upward momentum, a real estate career in Malaysia is no longer just a backup plan. It is becoming a serious upgrade. How to Become a Property Agent in Malaysia (Step-by-Step) Becoming a property agent in Malaysia is simpler than many people think. To legally practice, you need to register as a Real Estate Negotiator (REN) under BOVAEP, the Board of Valuers, Appraisers, Estate Agents and Property Managers. Step 1: Meet the basic requirementsYou must be a Malaysian citizen or permanent resident, at least 18 years old, with a minimum SPM qualification. No degree or prior real estate experience is required. Step 2: Complete the NCC courseThe Negotiator Certification Course covers basic property law, ethics and negotiation skills. After passing the assessment, you will receive a certificate recognised by BOVAEP. Step 3: Join a registered real estate agencyAs a REN, you cannot practise independently. You must be attached to a registered agency that will guide your training, registration and early career journey. Step 4: Get your REN tagYour agency will submit your application to BOVAEP. Once approved, your REN tag allows you to legally market, sell and rent properties in Malaysia. Step 5: Start building your careerFrom here, success depends on learning, follow-up, consistency and client trust. With commissions usually ranging from 2% to 3% per transaction, one successful deal can become a meaningful income milestone. That is why a real estate career in Malaysia is accessible, practical and worth considering for Gen Z Malaysians ready for a serious career reset. The Gen Z Advantage: Why Young Agents Win in Today's Market Here’s something the older generation of real estate agents may not always say out loud: young agents have a real advantage in today’s market. Content creation is second nature. Gen Z grew up making content. A well-shot property walkthrough on TikTok or a relatable Instagram Reel can reach thousands of potential buyers without spending a single ringgit on ads. And the right real estate marketing strategies can turn that content into consistent leads. They also understand today’s buyers better. Many Malaysian property buyers are now Gen Y and Gen Z, which means young agents often speak the same language, understand the same financial pressures and know what kind of communication feels trustworthy. Digital tools are another advantage. WhatsApp follow-ups, virtual tours, CRM apps, online listings and social media marketing are already part of how Gen Z lives and works.Today’s buyers can spot a scripted pitch quickly. Young agents who share their real journey, honest opinions and learning process can build trust faster than a polished sales script. Need proof? Read how Suthan went from career switcher to RM15 million in personal sales at just 26. Gen Z already makes up a major part of Malaysia’s population and workforce. Successful Gen Z real estate agents are not just the future of the industry. They are already here, building trust, generating leads and changing how property is marketed. What to Look for in a Real Estate Agency as a Young Agent Choosing your first real estate agency is one of the most important decisions you will make as a new agent. The right agency can shorten your learning curve, build your confidence and help you grow faster. Here’s what matters most when you are starting out. Real training, not just basic onboarding. A good agency does more than process your REN tag. It teaches you how to prospect, present, negotiate, follow up and close deals with confidence. Mentorship from people who have done it. The fastest way to grow as a real estate agent in Malaysia is to learn from experienced agents who are willing to guide you, not just compete with you. Take Ven Tee, for example. He went from a decade of frustration in banking to leading over 1,000 agents at IQI. That kind of story is possible when the right mentorship environment exists. Technology that supports your work. Lead management tools, marketing support, data insights and digital platforms can make a big difference, especially for young agents who want to work smarter. A culture that fits Gen Z. Autonomy, transparency and purpose matter. If the agency feels rigid, outdated or unsupportive, it may not be the right environment for your growth. Proof that young agents can succeed there. Don't just take the agency's word for it. See how Gen Z can genuinely benefit from a property agent career and look for an agency where that success is already happening. At IQI Global, agents are supported with training, mentorship, technology and a global network designed to help ambitious, digital-first agents build a real career in property, regardless of age or background. Is Real Estate Your Next Career Move? A career reset at 25 is not a setback. It is a decision to stop settling and start building a career that fits the future you actually want. For many Gen Z Malaysians, real estate is becoming one of the most serious paths forward. The entry barrier is accessible, the income potential is performance-based, and the digital skills you already have can become a real advantage in today’s property market. With the right agency, training and mentorship, the journey from beginner to confident real estate agent can move faster than many traditional career paths. Whether you are six months into a job that already feels draining or still figuring out your next move, a real estate career could be the pivot that changes everything. Ready to Make Your Career Reset Count? Real estate is more than a property career. It is a chance to build income, confidence, skills and long-term growth on your own terms. Whether you are exploring your first home, your next investment or a serious career move, IQI Global can guide you with the right people, tools and support. Connect with IQI Global today and take your next step in Malaysia’s property market. [custom_blog_form] Continue Reading: Where to Study Real Estate in Malaysia? Top Universities & Courses 2026 What is the Commission Structure for Real Estate Agents in Malaysia? How To Be a Property Agent in Malaysia in Just 5 Steps How Gen Z Can Benefit from a Property Agent Career Looking for a New Career? Check Out These 7 Highest Paying Jobs In Malaysia! References Kaur, S. (2026, May 18). Gen Z's short-term job mindset raises talent retention concerns. New Straits Times. https://www.nst.com.my/business/corporate/2026/05/1442004/gen-zs-short-term-job-mindset-raises-talent-retention-concerns Yang, O. J. (2026, January 11). Youths call it quits after 18 months. The Star. https://www.thestar.com.my/news/nation/2026/01/11/youths-call-it-quits-after-18-months Wong, J. (2025, November 17). Gen Y and Gen Z now dominate. StarProperty. https://www.starproperty.my/news/gen-y-and-gen-z-now-dominate/133816 IQI Global. (2026). How to be a property agent in Malaysia in just 5 steps. https://iqiglobal.com/blog/how-to-be-a-property-agent-in-malaysia-in-just-5-steps/ IQI Global. (2026). A guide to be a real estate agent Malaysia. https://iqiglobal.com/blog/a-guide-to-be-a-real-estate-agent-malaysia/ PropNex Malaysia. (2025). What's driving Gen Z & Millennials in Malaysia's property market? https://www.propnex.com.my/post/details/blog/gen%20z%20millenials%20real%20estate StarProperty. (2024, September 23). Navigating Gen Z's shift from renting to home ownership. https://www.starproperty.my/news/navigating-gen-z-s-shift-from-renting-to-home-ownership/129596 The Malaysian Reserve. (2024, April 22). Keeping up with Gen Z: Retaining Malaysia's future talent. https://themalaysianreserve.com/2024/04/22/keeping-up-with-gen-z-retaining-malaysias-future-talent/

21 May, 2026

Discover Johor’s 7 Most Richest Neighborhoods: Where Malaysia’s Southern Elite Choose to Live